Keller Group (LSE: KLR) — Position Review

The Quick Take

- Company: Keller Group (LSE: KLR) — the world’s largest geotechnical specialist contractor

- Thesis: A 165-year-old industrial that has just had its best year ever, sits in net cash for the first time in 25 years, is returning serious capital to shareholders, and is structurally exposed to four mega-trends (data centres, energy transition, infrastructure renewal, climate resilience) — yet still trades on a single-digit-times P/E

- Valuation: ~2,380p vs my fair value of 2,600p (≈9% upside) — the share has run hard in recent days but the in-flight £100m buyback is mechanically lifting fair value per share, and the structural drivers continue to validate the medium-term thesis

- Key risk: Cyclicality. Geotechnical contracting is project-based and follows the construction cycle; the 2024–2025 NA infrastructure boom has been the engine, and any meaningful US construction slowdown shows up here first

- Position: Built up over the past 12 months; meaningful weight in the portfolio

- Time horizon: 2–4 years

I’ve held Keller for some time and the stock has been one of the better performers in the portfolio — up roughly 60% in the last 12 months. The natural question after a run like that is whether the thesis is now in the price. My honest answer is mostly, yes. The structural tailwinds underneath the business are still building, the balance sheet has just transformed, and the capital-return programme alone provides a 12-month support. But the easy money on the operational turnaround has been made, the shares are at a fresh 52-week high, and from here it’s compound-and-collect rather than back-the-truck-up.

What Keller actually does

Keller is the world’s largest geotechnical specialist contractor — a description that does very little to convey what the business actually is. So let me put it more plainly: before anyone can build anything significant — a data centre, a battery factory, a port extension, a hospital, an airport runway, a high-rise — someone has to make sure the ground will hold the structure. That “someone” is increasingly Keller.

The business has been doing this for 165 years (founded 1860 by Johan Keller), employs around 10,000 people, and runs roughly 5,500 separate projects every year across five continents. It is a £3bn-revenue industrial that most retail investors have never heard of, partly because the work is — almost by definition — invisible the moment a project is finished. Nobody admires a building’s foundations.

The portfolio of techniques is genuinely broad: ground improvement (compacting or modifying soil so it can support what’s going on top), grouting (injecting cement or chemicals to stabilise the ground), deep foundations (piling), earth retention (holding back excavations), marine works (jetties, ports, sea defences), and instrumentation and monitoring. Most of these techniques are mature; the value Keller adds is in the engineering judgement to know which technique fits which ground condition, and the operational scale to execute thousands of these decisions a year reliably and safely.

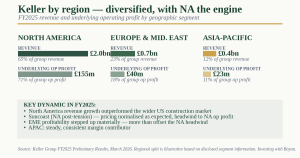

The three regions

Keller reports across three geographic segments, and the regional split is the right way to think about the business.

North America. The largest region by some distance, and the engine of the recent strong financial performance. Keller’s NA business has outperformed the wider US construction market through 2024 and 2025, driven by the unwinding of the US infrastructure investment programme and the structural surge in industrial construction (data centres, semiconductor fabs, EV battery plants, reshoring projects). Within NA, Suncoast — Keller’s post-tension systems business — had been a particularly strong contributor through 2023 and 2024, but pricing has been normalising as expected through 2025 and is now a modest profit headwind rather than a tailwind.

Europe and the Middle East (EME). Historically the most challenging region — UK and Continental European construction has been weak for several years, and Keller has been working through restructuring, site optimisation and pricing discipline. The good news: the work has paid off. EME profitability stepped up significantly in 2025 and more than offset the Suncoast normalisation in NA, which is what drove the record group result. The Middle East specifically has been a strong contributor as Gulf infrastructure programmes have ramped up.

Asia-Pacific (APAC). The smallest region and the most consistently profitable on an underlying basis. Australia in particular has been a durable contributor, with Singapore and other APAC markets adding incremental volume. APAC is not the headline-grabbing growth story but it is a steady margin contributor.

The geographic diversification is genuine and matters. A geotechnical contractor concentrated in any single market would be brutally cyclical. Keller’s three-region structure means that the rolling weakness in any one geography tends to be partially offset by strength in another, which is exactly what played out in 2025: NA softened on Suncoast, EME got materially better, and the group as a whole printed a record year.

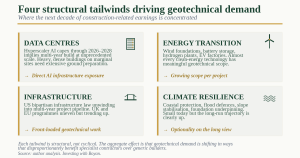

The structural demand story: where the next decade is going

This is the part of the story that I think deserves more attention than the recent operational turnaround.

Geotechnical contracting is, at first glance, a mature industry tied to the broader construction cycle. That framing misses something important. The composition of construction demand has been shifting in ways that disproportionately benefit specialist geotechnical contractors over generic builders, and the shift is structural rather than cyclical.

Data centres. Hyperscaler capex commitments for 2026–2028 imply a multi-year infrastructure build at unprecedented scale. Every new data centre site requires extensive ground preparation — these are heavy, dense buildings on often-marginal sites, and many are now being built in regions (Texas, Arizona, the US Midwest) where the soil conditions are demanding. Geotechnical work is one of the few industries where the AI capex cycle directly translates into project revenue without needing to bet on which chips win.

Energy transition. Offshore wind farms need monopile foundations driven into the seabed. Onshore wind needs heavy concrete foundations. Battery storage facilities need ground improvement. Hydrogen plants need specialist grouting. EV battery factories — which are typically very large and very heavy — need extensive deep foundations. Almost every single technology in the energy transition has a meaningful geotechnical scope item that didn’t exist twenty years ago.

Infrastructure renewal. US infrastructure spend has structurally increased post the bipartisan infrastructure law and is unlikely to revert quickly regardless of political administration. UK and European infrastructure programmes are more uneven but the medium-term direction is up. Bridge, road, port, rail and airport programmes are all geotechnical-intensive at the front end.

Climate resilience. Coastal protection, flood defences, slope stabilisation against landslide risk, dam strengthening, foundation underpinning for buildings sinking on shifting soils — all geotechnical work, all in growing demand as climate-related ground instability becomes a larger and more visible problem. This is currently a small slice of revenue but the long-run trajectory is clearly up.

The honest framing is that Keller doesn’t need to win share to grow — it just needs to maintain its position in markets where the underlying demand is structurally accelerating. That’s a fundamentally different (and easier) growth profile to a generic construction services company.

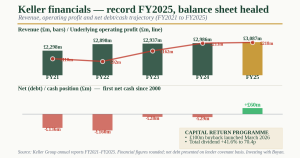

Financial shape: from leverage clean-up to capital returns

The financial transformation under James Wroath (CEO since 2020) is genuinely impressive and is worth understanding in its own right.

Revenue. Grew from ~£2.2bn in 2020 to £3.09bn in FY2025. Roughly 7% CAGR through a period that included Covid disruption, supply-chain problems and rising interest rates.

Underlying operating profit. £218.2m in FY2025, up 2.6% on the prior year, underlying operating margin of 7.1%. The margin number doesn’t sound exciting until you realise that this is a contracting business, where 7%+ at scale is quite respectable, and the trajectory is up — H1 2024 ran 7.6%, H1 2025 ran 7.0%, full year 2025 came in 7.1%. The medium-term goal is 8–10%, which is plausible if the EME margin progression continues.

Balance sheet. This is the headline. Keller closed FY2025 with net cash of £59.7m — the first net cash position in 25 years. The balance sheet improved by £89.2m over the year despite the £25m H1 buyback investment. To put that in context: this is a company that historically ran with £150–250m of net debt, often pushing against covenant headroom in difficult years. The fact that it’s now net-cash is a structural change in the equity story.

Capital returns. The £50m buyback initiated in early 2025 is now substantially complete. A new £100m buyback programme launched in March 2026 — Investec executing the first £50m, Peel Hunt the second £50m, expected to conclude by end-March 2027. At ~£1.5bn market cap that’s around 6.7% of the share count being retired in one year. The total dividend was raised 41.6% to 70.4p, a yield around 3.3% at current prices. Total capital return for FY2025 — dividend plus buyback — equates to roughly 10% of market cap.

Cash conversion. Working capital reverted to a more normal pattern in 2025 after particularly strong performance in 2023–24. H1 2025 saw a working-capital outflow as the business invested in projects, but H2 reversed it and the full-year cash flow was strong enough to fund the buyback, the dividend and still build the net cash position.

This combination — record P&L, record balance sheet, accelerating capital returns — is what’s driven the share price up over 50% in the last 12 months. The trick now is whether it can compound from here.

Valuation

At ~2,380p, Keller’s market capitalisation is approximately £1.6bn on roughly 69m shares outstanding. FY2025 underlying diluted EPS came in around 220p, putting the trailing P/E at about 10.8x. Consensus FY26 EPS is around 226p, putting forward P/E at about 10.5x. Trailing dividend yield is 3.0%, capital-return yield (dividend + buyback) is around 9–10%.

For a business with these characteristics — net-cash, returning ~10% of market cap a year to shareholders, structurally exposed to four mega-trends, and just printed a record year — a 10–11x forward P/E is, frankly, still modest. UK construction services peers typically trade in the 10–13x range; international engineering services in the 13–16x range; specialty industrials with similar quality metrics often higher.

My fair-value framework lands like this:

- Bull case (~2,800–3,300p, 18–39% upside). EME margin progression continues and the group margin steps toward 8%+. NA holds up despite Suncoast normalisation. The data-centre and energy-transition order book builds visibly. The market re-rates the equity to a 13–14x forward P/E on a growing earnings base. The ongoing buyback continues to retire stock at attractive levels.

- Base case (~2,500–2,700p, 5–13% upside). EPS holds around 225–235p with modest growth. Multiple holds at 11–12x on the increasingly visible quality of the business. Buyback support keeps a floor under the share price. Dividend continues to compound.

- Bear case (~1,600–1,900p, 20–33% downside). US construction softens materially as data-centre capex digests. EME momentum fades. Suncoast pricing pressure accelerates. Multiple compresses back to 8–9x on a flat earnings base.

Probability-weighting (35% bull / 50% base / 15% bear) gives a central fair value of approximately 2,600p on a 12–18 month view — roughly 9% upside from current levels. Add the ~3.0% dividend yield and 6.5% buyback yield and the all-in expected return is in the high-teens on a one-year view, even before any further multiple expansion.

I should be honest about what the recent price action means. When I first drafted this piece a few days ago the shares were ~2,200p and the upside to my then-central fair value of 2,500p was ~14%. Two factors warrant lifting my central fair value modestly to 2,600p as the shares have rallied. First, the £100m buyback is now executing meaningfully — at the current pace the share count will reduce by around 6.7% over the next 12 months, which mechanically lifts fair value per share even with unchanged enterprise value. Second, the shareholder probability distribution has shifted: the rally itself, combined with continued operational momentum, is mild evidence that the bull case is the more likely outcome, and I’ve nudged the probability weighting from 30/50/20 to 35/50/15. The fundamental case has not changed; what has changed is that the buyback mechanics are now meaningfully shifting the per-share maths and the bull-case path looks marginally more probable. New money at 2,380p is paying close to fair value for execution rather than buying at a discount. Existing holders (myself included) are now in a “trim or hold” decision rather than an “add” decision, with the case for holding resting primarily on the capital-return yield and the medium-term structural drivers playing out over the 2–4 year time horizon.

This is not a screaming-cheap thesis. It is a “good business, fair price, with meaningful capital-return tailwinds” thesis — closer in shape to my Volex view than to MS International or Ondine. The shares have done a lot of the work already; from here it’s about whether the structural tailwinds continue to translate into earnings, and whether the buyback support holds the share price through any cyclical wobble.

Key risks

I’d be misleading anyone if I left these out:

- Construction cyclicality. Geotechnical contracting is project-based and follows the construction cycle. A meaningful US construction slowdown would show up here first. The 60%+ share-price gain in the past 12 months is partly a function of where we are in the cycle — and cycles always end.

- NA concentration. Despite the geographic diversification, North America remains by some distance the largest profit pool. Any combination of weaker infrastructure spend, softer industrial construction, or more aggressive Suncoast pricing pressure has a disproportionate impact on group earnings.

- Project-execution risk. Geotechnical work is by nature high-risk — ground conditions are never fully knowable until you start digging, weather affects everything, and a single major project loss can move the half-year numbers. Keller manages this with rigorous bid discipline and contingency, but the risk is structural to the industry.

- FX exposure. Reports in GBP but most revenue is non-GBP (predominantly USD). Sterling strength against the dollar is a translational headwind — the FY2025 numbers were achieved despite an FX drag.

- Margin already at the high end of recent history. The 7.1% group operating margin is towards the top of the post-2018 range. Margin expansion from here requires the EME progression to continue without NA giving back what’s been gained.

- Multiple compression in a risk-off environment. Although the forward P/E is undemanding, contracting businesses tend to de-rate sharply when construction cycles turn. The current 9–10x could compress to 7–8x in a meaningful downturn.

What I’m watching from here

Three concrete operational tests will define the next 12 months:

- EME margin progression continues in the H1 2026 print (August 2026). If the European and Middle Eastern profitability uplift was a one-year recovery rather than the start of a multi-year journey, the bull case weakens materially.

- NA order book holds up despite Suncoast pricing normalisation. Watch the commentary on the data-centre, semiconductor and battery-plant pipeline specifically — this is where the structural demand story has to keep showing up in real orders.

- The £100m buyback executes on schedule by end-March 2027. This is the clearest near-term technical support for the share price. A continuation announcement in 2027 would tell you the board still sees the shares as undervalued.

If those three boxes tick, this becomes a different conversation — the multiple should re-rate towards the upper end of my bull case. If NA softens before EME has fully delivered, the share price gives back a chunk of the recent gains. The position is sized to be tolerant of either outcome, but I’m leaning toward the structural case continuing to deliver.

In summary, Keller is a genuinely good business that has just had its best year ever. The shares have responded accordingly — but the combination of a 10–11x forward P/E, a net-cash balance sheet, a ~9–10% combined capital-return yield, and structural exposure to data centres / energy transition / infrastructure / climate resilience is still attractive even after the run. It is not the asymmetric setup it was a year ago, and after the recent rally it is now within touching distance of my central fair value. It is a high-quality compounder paying you handsomely to wait, and that fits a particular slot in the portfolio that I’m happy to keep filled — though I’d be more cautious about putting fresh money in at these levels.

Disclosure: I hold a position in Keller Group at the time of writing. This is not investment advice — always do your own research. Read the full disclaimer at investingwithboyan.com.

If you found this useful, more analysis is available at investingwithboyan.com — or subscribe via the form in the sidebar to get new pieces straight to your inbox.