MS International (AIM: MSI) — Initiation of Coverage (Refresh)

The Quick Take

- Company: MS International (AIM: MSI) — a UK family-controlled engineering group built around MSI-Defence Systems, a tier-one supplier of naval gun systems and counter-drone air defence to global navies and land forces, with three legacy civilian divisions (Forgings, Petrol Station Superstructures, Corporate Branding) now formally being readied for disposal

- Thesis: A debt-free, cash-generative defence compounder mispriced as a sleepy AIM micro-cap; the Terrahawk Paladin counter-drone franchise is now combat-proven in Ukraine and operationally fielded in Jordan, on top of a sole-source US Navy gun-mount business and — most recently — selection by the Royal Canadian Navy for the 15-ship River-class destroyer programme

- Catalyst: Imminent disposal of the three non-core divisions to trade buyers, leaving a pure-play defence equity that should re-rate on a cleaner multiple

- Valuation: ~1,600p vs my sum-of-the-parts central case of ~2,000p (≈25% upside on base case, with optionality on Middle East / Gulf order flow and a successful divisional sale taking that materially higher)

- Key risk: Defence revenue recognition is lumpy by design — H1 FY26 PBT slipped slightly on order timing, and corporate communications remain so notoriously thin that material platform wins regularly leak via third parties before the company itself acknowledges them

- Position: Built progressively from the mid-triple-digits through 2024 and into 2025; now my fourth-largest holding and a cornerstone of the portfolio

- Time horizon: Multi-year — this is an operational compounding story with a corporate simplification catalyst, not a single-event trade

I built my MSI position progressively over 2024 and 2025, on average somewhere around 900–1,100p. The shares have since been on a tear — from a 52-week low of ~860p to a recent ~1,600p, a more-than-80% move that flatters the entry but also raises the natural question every investor should ask after a re-rating: is this still a buy, or am I just holding?

I think it remains a meaningful holding — but for materially different reasons than when I started buying. The original thesis was simple: a forgotten Yorkshire engineering family business quietly minting cash, with a defence division the market hadn’t woken up to. That part is now visible to anyone who can read a P&L. What has shifted my conviction up rather than down at these levels is the structural story: a long-running internal review has now formally concluded with the decision to focus the group on Defence and dispose of the three civilian divisions, the company is — for the first time in living memory — actively courting institutional capital with site visits to its Norwich facility, and the operational momentum continues to compound (Ukraine, Jordan, a fresh US Navy contract, and most strikingly the Royal Canadian Navy’s adoption of the Mk 38 Mod 4 for its 15-ship River-class destroyer programme).

That last item, you should note, was confirmed not by MSI but by a Canadian naval blog. Which is its own kind of signal, and one I’ll come back to.

What MSI actually does

MS International is, by some distance, the most delightfully bizarre conglomerate listed on the London Stock Exchange. If you pitched this corporate structure to a modern MBA class you would be politely escorted from the room. The group has, until now, run four entirely unrelated divisions: Defence and Security, Forgings, Petrol Station Superstructures, and Corporate Branding. There are precisely zero operational synergies between forging fork-arms for industrial trucks, building canopies for petrol stations in Lincolnshire, putting up corporate signage, and manufacturing 30mm automated chain guns for sovereign militaries.

For decades this was simply how the chairman ran the business — and the structural complexity is exactly the kind that algorithmic screeners find difficult to categorise, and which traditional institutional capital does not have the mandate to wade into. That has been, in equal measure, both the source of the persistent mispricing and the headache of every analyst trying to value it.

What is changing — and changing now — is that management has finally agreed to do something about it.

The disposal: from conglomerate to pure-play

In the H1 FY26 interim statement (January 2026), the chairman stated explicitly that 2025 was “arguably the most significant year for the business since its formation,” because it concluded a two-year internal review with the decision to focus the group on Defence and Security and dispose of the three non-core divisions. That is not boilerplate — it is the most consequential strategic announcement MSI has made in decades, and it changes the shape of the equity story.

The disposal process to date has had two phases:

- Spring 2025: market-test phase. The board tested external interest in Forgings, Petrol Station Superstructures and Corporate Branding. The company received “encouraging interest, but mainly from financial buyers” — i.e. private equity. Sensibly, management chose not to transact at private-equity-only pricing.

- 2026: trade-buyer phase. The stated objective for this calendar year is to extend the dialogue to trade buyers for the three businesses. This is meaningfully more interesting valuation territory: trade buyers pay for synergies and strategic fit; financial buyers pay for IRR. A trade sale tends to clear at a 20–40% premium to a financial sale for businesses of this profile.

The trade-buyer angle has materially better optionality than I think the market has yet absorbed, particularly because of one detail that is easy to miss in a quick read of the disclosures.

MSI-Forks (the Forgings division) has US manufacturing. Specifically a manufacturing plant in South Carolina, opened in 2017 to serve the American market, alongside facilities in the UK and Brazil. In a tariff environment where US industrial buyers are actively paying premiums for US-domiciled manufacturing capacity to avoid import duties, that footprint is genuinely strategic. A US trade buyer evaluating MSI-Forks is not just buying a profitable forgings operation; they are buying installed, operational, ANSI-compliant US production capacity that they can plug straight into their own supply chain. The Brazil facility is a useful secondary asset for Latin American distribution, and the UK plant carries the Doncaster heritage.

The Petrol Station Superstructures business has its own UK and Polish operations and is a viable acquisition for a European forecourt-services consolidator. Corporate Branding is small, clean, and the easiest of the three to dispose of to a UK signage / branding peer.

I think a realistic aggregate disposal value sits in the £40–70m range, depending on how aggressively the trade-buyer process runs and how much of the Forgings premium MSI can capture. That is a meaningful proportion of the current £261m market cap, and crucially it would be paid in cash to a debt-free company. The capital allocation question — special dividend, buyback, accelerating Defence capex — then becomes the next thing to watch.

But the bigger valuation effect is qualitative rather than arithmetic: once the disposal completes, MSI is a pure-play defence equity, and the entire reason for the historic structural discount goes away.

Four divisions, one story (for now)

Even before the disposal completes, it is worth being honest about how the value actually splits today.

Defence and Security is the engine. MSI-DS designs and manufactures stabilised naval gun systems (the Seahawk family), the Mk 38 Mod 4 / MK88 Mod 4 stabilised gun mounts for the US Navy, and the Terrahawk Paladin very-short-range air-defence system. By my estimate, Defence accounts for roughly three-quarters of group operating profit at run rate.

Forgings is the legacy heritage — fork-arms for industrial trucks and open-die forgings, manufacturing in Yorkshire, South Carolina and Brazil. Profitable, cyclical, and (as discussed above) more strategically interesting from a US trade-buyer perspective than the multiple a financial buyer would put on it.

Petrol Station Superstructures designs, builds and maintains forecourt canopies, with UK and Polish operations. Not a growth category, but profitable and asset-light from the group’s perspective.

Corporate Branding is small, mostly stable, serves blue-chip UK corporate signage clients.

The internal logic in keeping these together has run its course. The capital, management bandwidth and shareholder discount they have been costing the group meaningfully exceeds the cash they generate. The disposal is the right call — twenty years late, perhaps, but the right call.

The asymmetric economics of drone warfare

To understand why the residual Defence pure-play is genuinely under-priced, you have to understand what has happened to the air-defence market over the last three years.

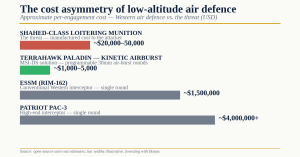

The proliferation of cheap, weaponised commercial drones and loitering munitions — most prominently the Iranian-designed Shahed family — has comprehensively inverted the economics of low-altitude air defence. A Shahed-style loitering munition costs the manufacturer something on the order of $20,000–50,000. The traditional Western response has been to fire a sophisticated surface-to-air missile at it. A single ESSM costs approximately $1.5–2m. A Patriot PAC-3 round is several million.

Firing a $2m interceptor at a $20,000 drone is, to put it gently, a spectacular way to bankrupt a defence ministry inside three months. Ukraine is now the largest live-fire laboratory in the world for what happens when you actually have to defend critical infrastructure against drone swarms at scale, and the lesson coming out of it is unambiguous: the modern battlefield needs a mobile, sensor-agnostic, kinetic kill system that can physically shred drones out of the sky for pennies on the dollar.

The market for short-range counter-UAS systems is forecast to grow at over 20% annually through the end of the decade. The customer list is: every NATO member, every Gulf state, every country with critical infrastructure within drone range of an unfriendly border. That is a very long list.

Enter the Terrahawk Paladin

Terrahawk Paladin is MSI’s answer. It is a deployable, palletised air-defence system built around a 30mm Mk 44 Bushmaster II autocannon, integrated with MSI’s own SATOS sighting system (thermal sensor, laser rangefinder, automatic target tracking) and AESA-radar fire control supplied by Polish partner Advanced Protection Systems. It uses programmable air-burst ammunition that creates a wall of shrapnel at precisely the right moment to destroy low-flying targets out to about 2km. It can be operated by a crew of two, integrates with existing radar systems, and crucially is derived from MSI-DS’s Seahawk family of naval gun systems — so the underlying engineering is mature, not speculative.

What makes this particularly valuable is that Terrahawk Paladin is no longer a trade-show concept. It is fielded hardware, used in earnest, by sovereign customers, in active threat environments. Three operational waypoints have shifted the system from “interesting product” to “validated platform” in a way the market has, in my view, only partially digested:

- The UK gifted Terrahawk systems to Ukraine through the International Fund for Ukraine, with the system included in a >£100m support package administered by the UK MoD on behalf of the IFU executive panel (UK, Norway, Netherlands, Denmark, Sweden). There is no harder operational reference than “in active use against Russian Shahed strikes on Ukrainian critical infrastructure”.

- Royal Jordanian Air Force operational deployment was confirmed publicly during Exercise Sky Shield in September 2025, with King Abdullah II in attendance. Two Terrahawks were deployed during the exercise, operated by RJAF air-defence personnel, with the JAF crediting the system with the kinetic kills demonstrated against simulated drone swarms crossing the eastern border.

- Earlier UK MoD orders for British Army usage, secured in 2022 and expanded since, established the domestic credibility that other foreign militaries look for before procurement.

For a Gulf state currently watching Houthi or Iranian-aligned drone fragments land on its oil infrastructure, the procurement decision is not theoretical. The threat is active, the budget is allocated, and the question is which system to buy. Combat-validation history matters disproportionately in defence procurement, and Terrahawk now has the kind of operational dossier its competitors simply do not.

The naval business: sole-source economics, and a quietly transformational platform win

While Terrahawk Paladin is the headline-generating optionality, the bedrock of MSI’s defence valuation has historically been its position with the US Navy.

MSI’s South Carolina-based defence subsidiary, MSI-Defence Systems US LLC, manufactures the stabilised gun mounts that the US Navy designates as the Mk 38 Mod 4 (also referenced as MK88 Mod 4). In late 2025, that subsidiary secured a further $34.5m sole-source contract for additional gun mounts, maintenance modules and on-board repair parts, with deliveries running through December 2026. This came on top of the prior year’s procurement programme being formally awarded in October 2025 following a “Request for Purchase” from the US Navy.

The phrase that matters in those announcements is “sole source basis.” Once a weapon system is integrated into the US Navy’s fleet — qualified, certified, trained on, spare-parts inventoried — the switching costs are astronomical. You do not casually swap out the primary stabilised gun mount on a US Navy surface combatant.

But the much more interesting development is what has happened outside the US Navy.

In late March 2026, the Royal Canadian Navy publicly unveiled the latest design model of its future River-class destroyer — the Canadian Surface Combatant (CSC) programme, intended to deliver up to 15 guided-missile destroyers to replace the retired Iroquois class and the ageing Halifax frigates. The first ship, HMCS Fraser, is already under construction at Irving Shipbuilding. Among the design changes confirmed in the unveiling: the close-in weapon system, originally specified as Italian Leonardo Lionfish 30mm mounts, has been replaced by the British-made MSI-DS Mk 38 Mod 4 — the same system already in service with the US Navy.

To be clear about what this means: MSI has just been confirmed as the close-in gun system supplier for what is one of the largest Western surface-combatant programmes of the decade — a 15-ship build with a multi-decade operational life and a recurring spares-and-maintenance tail that will last well into the 2050s. This is a platform win comparable in size to anything else in MSI-DS’s order book. It is also a strong validation of the Mk 38 Mod 4 as a NATO-standard close-in weapon, with obvious read-across to other Type 26 derivative programmes (the Royal Navy’s own Type 26 frigates and the Australian Hunter class).

I cannot find an MSI press release announcing this. I have looked. The platform selection was confirmed by the Royal Canadian Navy at a public unveiling at National Defence Headquarters in Ottawa, picked up by NavyLookout, the Canadian Naval Review, ReadyAyeReady, and the broader defence press — but as of this writing, MSI shareholders have not had a formal company communication about it.

This is a genuinely strange way to run an investor relations function for a listed company that has just won material business. But it is also entirely consistent with how MSI has operated for decades, and it is — surprisingly — improving.

The communications problem (and what is changing)

If you want a crisp summary of what has historically deterred institutional capital from MSI, it is this: the company has had no analyst coverage, no investor day, no quarterly call, no proactive announcement around major platform wins, and an AGM in Yorkshire that one private investor on a forum joked about needing to budget £200 of British Rail tickets and gin-and-tonics for. The chairman’s interim and final statements have, until very recently, been almost the only direct communication shareholders received.

Set against the operational story above, that is genuinely costly. It is a textbook example of a high-quality business whose mispricing is partially a function of its own reluctance to engage with the capital markets.

What is encouraging — and what has been understated in most write-ups I’ve seen — is that this is now changing. Three concrete signals:

- New institutional shareholders. The chairman noted in the H1 FY26 interim that 2025 saw “several new institutional shareholders invest in the business.” This is not a description of a company hostile to institutional capital; it is a description of one that is actively cultivating it for the first time.

- Norwich site visits for institutional investors. The H1 FY26 interim statement confirms that MSI has been organising institutional investor visits to the Norwich Defence and Security facility, with feedback described as “very encouraging.” For anyone who has covered this name, this is a near-revolutionary change. Site visits are the single highest-ROI form of corporate access for a small-cap defence business — letting a fund manager actually see the production line, the engineering, the inventory build, and meet the operational team. The fact that MSI is now doing this is a meaningful signal of genuine intent to broaden the shareholder register.

- Stated intent to expand investor liaison. The chairman explicitly states the intent to “expand our liaison with existing and potential investors” as interest grows.

This is still nowhere near best-in-class IR. The Canadian River-class platform announcement should have been a formal RNS the day after the RCN unveiling. The Mid-East order pipeline should be communicated more crisply. But the trajectory is clearly toward more, not less, engagement — and combined with the conglomerate cleanup, that should structurally reduce the discount the equity has historically traded at.

The strategic balance sheet: hoarding metal

One of the more interesting signals in MSI’s recent results is what management has been doing with the cash pile.

At the FY25 year-end (April 2025), the group held £27.78m in cash, down meaningfully from £42.68m the prior year. At H1 FY26 (October 2025) closing cash was lower again, at £14.23m. On a superficial read, that looks like cash burn. It is not.

What management has actually been doing is deliberately deploying that cash into capacity expansion and a substantial increase in raw material and component inventory. £3.58m has been spent on the Norwich facility expansion over the past two years alone, and inventory positions have built materially. The logic is straightforward: in the defence sector today, the binding constraint on order conversion is not demand — it is supply chain. If a sovereign nation needs counter-drone systems fielded in eight weeks rather than eighteen months, the supplier who can manufacture and ship is the supplier who wins the order.

By pre-positioning inventory and expanding production footprint, MSI is effectively buying future market share with its balance sheet. Even after this heavy investment, the group remains debt-free. Layer on the prospective cash inflow from the divisional disposals, and the funded capacity to scale Defence is well in excess of what the current run-rate would suggest.

Financial shape: H1 wobble, structural strength

The FY25 numbers (year to April 2025) were genuinely excellent: revenue of £117.50m (up from £109.58m), pre-tax profit of £20.05m (up 27% YoY), pre-tax margin of 17%, basic EPS of 90.0p. Those are the numbers a well-run, asset-light, defence-tilted engineering business should print, and they validated the buy-and-hold thesis.

The H1 FY26 interim results, published in January 2026, were softer — and worth being honest about. Revenue for the six months to 31 October 2025 came in at £55.81m (vs £54.72m), broadly flat year-on-year, with PBT of £8.47m (vs £8.77m). The chairman attributed the flat performance to timing of defence orders and the constraint that revenue is only recognised when performance obligations are satisfied — not to any underlying demand softness. He had already guided to a slower current financial year in the prior FY25 statement, so the print was not a surprise.

Defence revenue recognition is genuinely lumpy. A £20m programme can slip a quarter or two and the half-year numbers will look pedestrian even when the underlying order book is accelerating. The market is occasionally unforgiving of this — the share has had drawdowns of 17% inside a quarter on no fundamental news — and if you are not prepared to sit through that volatility you should not own this stock at meaningful position size.

The structural metrics are doing their job: net cash, very high returns on capital (ROE ~25%, ROIC ~48% on the trailing year), and a dividend covered nearly four times by earnings. Trailing twelve-month figures broadly aggregate to revenue of ~£118m and net profit of ~£14m. The basic EPS run-rate of around 86p on the trailing twelve months puts the stock on roughly 18.5x trailing earnings at 1,600p — not a screaming-cheap multiple, but it sits against an order book pipeline, an export catalyst, the River-class win, and a multi-year defence spending cycle.

Valuation: a disciplined sum-of-the-parts, with a disposal kicker

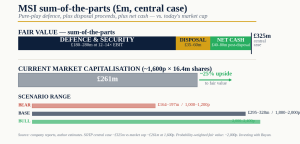

Pricing MSI requires you to separate the residual Defence pure-play from the disposal proceeds.

Residual Defence and Security (post-disposal). Assume Defence runs at ~£15m of EBIT on a TTM basis, with a credible path to £20–25m as Norwich capacity scales and Terrahawk export orders convert. Defence peer multiples — Cohort, Avon Protection, the broader UK defence small-cap cohort — sit in the 12–14x EBIT range. MSI-DS’s economics (sole-source US Navy, combat-validated counter-drone IP, River-class platform position, net-cash) sit at the strong end of that peer set. That gets you to £180–280m of standalone Defence value depending on whether you use trailing or forward EBIT, and what multiple you assign for the increasingly visible growth profile.

Disposal proceeds. Aggregate sale value for the three civilian divisions in a trade-buyer process: I think a reasonable range is £40–70m, with the upside skewed by what a US industrial buyer pays for the MSI-Forks operation given its US manufacturing presence in the current tariff environment. Net of disposal costs and tax leakage, perhaps £35–60m of cash to the parent.

Net cash and balance sheet. Pro-forma net cash position post-disposal, assuming continued working capital normalisation: ~£40–80m depending on disposal timing and capital allocation choices.

Sum-of-the-parts. Aggregate fair value range of approximately £250–360m, or 1,500–2,200p per share on 16.4m shares outstanding. The mid-point of that range — call it ~2,000p — is approximately 25% above where the stock trades today.

The dynamic case beneath the static numbers has three drivers:

Bull case (2,000–2,400p central, 25–50% upside). Terrahawk converts two or three meaningful Gulf state orders over the next 18 months; the Mk 38 Mod 4 backlog scales as the US Navy continues fleet upgrades and as the Canadian River-class programme begins fitting; the divisional disposals complete at the upper end of the range; group EBIT (post-disposal, on the residual Defence business) grows toward £25–30m as the inventory build converts into delivered revenue; and the market re-rates a now-pure-play defence equity onto a forward multiple closer to 14–15x growing earnings.

Base case (1,800–2,000p, 12–25% upside). Steady drumbeat of defence wins, civilian divisions sold for a reasonable but not heroic price, residual Defence trades on a defence-peer multiple. This is essentially “compound at 10–15% a year while collecting the dividend” plus a one-time uplift from the corporate simplification.

Bear case (1,000–1,200p, 25–37% downside). A combination of continued lumpy revenue recognition, a slowdown in defence procurement enthusiasm if the Ukraine conflict de-escalates faster than expected, multiple compression as the AIM defence trade cools, and disposal processes that drag through 2027 without clearing. This is plausible — markets are mean-reverting — and it is the scenario for which the position sizing has to be tolerant.

Probability-weighting (40% bull / 45% base / 15% bear) gets me to a central fair value of approximately 2,000p on a 12–24 month view. With the disposal catalyst now formally in motion, I think the asymmetry is genuinely better than it was when I started buying.

Why the market still gets this wrong

The structural reasons MSI continues to trade at a discount to where it should are worth being explicit about:

- AIM micro-cap classification automatically excludes the stock from the mandate of a meaningful slice of UK institutional capital.

- The “messy conglomerate” optics — petrol stations and forgings sitting next to weapons systems — make the stock genuinely difficult for screen-driven investment processes to categorise correctly. This is exactly what the disposal addresses.

- No analyst coverage of substance. There is no published sell-side model an institutional generalist can pick up.

- Sub-optimal communications. Major platform wins (River-class) are not formally announced; the IR cadence has historically been minimal. This is what the Norwich visits and broader institutional courtship are starting to address, but it remains a real headwind.

- Family control. The Bell family chairmanship is a feature of the business — long-horizon thinking, conservative finance, no quarterly games — but it is also a deterrent for institutional capital wanting greater accountability.

The first three of these are structural and will persist; the second two are actively being worked on by the board. The combination of “structural discount narrowing + operational story compounding + disposal catalyst” is what makes the risk/reward genuinely better today than it was at half the price.

Key risks

I would be misleading anyone if I left these out:

- Defence revenue lumpiness. H1 FY26 was the latest reminder. Order timing slippage is the norm, not the exception, and a single half-year miss can drive sharp drawdowns on a stock with this liquidity profile.

- Family control / governance. The Bell family runs the business with very long-term horizons, which I view as a positive — but governance critics are not wrong to point out that capital allocation, dividend policy, and disclosure are all set by an executive chairman who owns enough to do as he pleases.

- Disposal execution risk. The corporate cleanup is the right strategic call, but the trade-buyer process for the three civilian divisions could take 12–18 months to clear — or longer — and discount-rate compression around the disposal timing is a real factor for the equity.

- AIM small-cap liquidity. Sub-£300m market cap with a constrained free float (family shareholdings absorb a significant chunk). Position sizing matters more here than for liquid mid-caps; exit on a bad day can be costly.

- Geopolitical reversal. The defence procurement cycle is being driven by an active war in Europe and active drone threats in the Middle East. A meaningful de-escalation in either theatre would compress the multi-year procurement assumption that underpins the bull case.

- Communications continue to lag operations. The Canadian River-class confirmation is a recent example. If material wins continue to leak through third parties before the company acknowledges them, the share price reaction tends to lag and capital rewards the patient holder rather than the short-term trader. That is fine for me; it is less fine for the marginal new buyer.

- Working capital risk. The deliberate inventory and capacity build is the right strategic move, but if order conversion slips materially the working capital balance will look stretched.

What I’m watching from here

The next twelve months will be defined by four concrete operational and corporate tests:

- Conversion of the inventory build into recognised revenue in the H2 FY26 results (mid-2026). If the slower H1 was genuinely a timing artefact, the second half should show acceleration — and the FY26 numbers in aggregate should at minimum hold the FY25 baseline.

- Visible progress on the disposal of Forgings, Petrol Station Superstructures and Corporate Branding — ideally with at least one division formally sold to a trade buyer at a credible multiple. The MSI-Forks disposal is the one I’d watch most closely for the US-tariff angle.

- At least one further Middle East / Gulf Terrahawk order announcement. Jordan was the proof-of-concept; one sizeable export order in the next 12 months would meaningfully validate the bull case.

- Continued visibility on the Mk 38 Mod 4 platform pipeline — confirmation of the Canadian River-class commercial terms, follow-on US Navy tranches, and any incremental NATO-standard integration wins.

If those four things deliver — even broadly — this becomes a different conversation, and the stock should move toward the upper end of the bull case. If the disposal stalls and Terrahawk export momentum fails to materialise, the static fair-value range applies and the stock is a hold-not-add. The position is sized to be tolerant of either outcome, but I am leaning toward the operational case continuing to deliver.

In summary, MSI remains a cornerstone holding for a portfolio looking for genuine quality compounding in a structurally mispriced corner of the market. It is debt-free, generates extraordinary returns on capital, has a defensible moat in two distinct defence niches, has just been confirmed on the largest Canadian surface combatant programme in a generation, and is run by a management team patently focused on the next decade rather than the next quarter — and that team is, for the first time, doing the work to make the equity story legible to institutional capital. It will not win prizes at a Silicon Valley summit. The investor relations philosophy is improving but still not where it should be. The AGM is in Yorkshire. But when a small-cap engineering business is generating £20m of pre-tax profit, sitting on net cash, building combat-validated weapons that NATO, Canada and Gulf states are actively procuring, undertaking a corporate simplification that should structurally re-rate the multiple, and trading at a sum-of-the-parts that ignores most of the optionality — the slick PowerPoint is, frankly, optional.

Disclosure: I hold a position in MS International at the time of writing. This is not investment advice — always do your own research. Read the full disclaimer at investingwithboyan.com.

If you found this useful, more analysis is available at investingwithboyan.com — or subscribe via the form in the sidebar to get new pieces straight to your inbox.