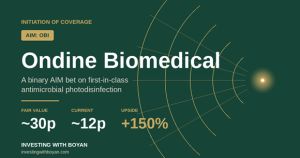

Ondine Biomedical (AIM: OBI) — Initiation of Coverage

The Quick Take

- Company: Ondine Biomedical (AIM: OBI) — Canadian life-sciences group commercialising Steriwave®, a non-antibiotic nasal photodisinfection therapy

- Thesis: Asymmetric, catalyst-driven AIM venture bet on the first FDA-approvable nasal decolonisation product, anchored by HCA Healthcare’s strategic alignment as trial partner, equity holder and intended commercial channel; UK adoption via Mölnlycke supplies validation but is not the active engine

- Valuation: ~12p vs my probability-weighted fair value of ~30p (≈150% upside on base case; binary skew much wider in either direction around the LANTERN data)

- Key risk: LANTERN Phase 3 readout is binary; a miss or weak result would likely halve the equity and force further dilutive funding

- Position: Built through 2025 mostly at ~12p; high-conviction holding sized for the asymmetric pay-off

- Time horizon: 12–18 months, dominated by LANTERN top-line (Spring 2026) and FDA pathway

I built my Ondine position through 2025, mostly around 12p. The shares had drifted from the high teens last summer to roughly that level and have stayed there, capped most recently by a £5m placing at 12p to fund the FDA submission. The entry has not been pretty — but the asymmetry into the LANTERN readout is, in my view, more attractive now than at any point since I started looking at the name.

This is a different kind of holding to most names in the portfolio. It is not a quietly compounding small-cap with a fortress balance sheet. It is a binary biotech bet with cash runway only through Q4 2026 and a single, large clinical trial that will more or less determine the next five years of the equity. The underlying technology, the institutional alignment around it (HCA Healthcare, in particular), and the price I am paying have given me enough conviction to run this as a meaningful holding into the data — though biotech is biotech, and discipline here is about recognising that conviction is not the same as certainty.

What Ondine actually does

Ondine is a Canadian life-sciences company that has commercialised a non-antibiotic way of killing pathogens in the nose — fast, painlessly, and crucially without breeding the resistance that is steadily eroding the world’s antibiotic arsenal. The lead product, Steriwave®, is a single five-minute pre-surgical treatment that destroys bacteria, viruses and fungi inside the nasal passage, the principal reservoir for the bugs that go on to cause surgical site infections (SSIs) and other healthcare-associated infections (HAIs).

The mechanism is elegant. A photosensitive agent is swabbed into each nostril, then activated by a specific wavelength of red light. The activation triggers an oxidative burst that physically destroys the pathogens — so quickly (sub-20 seconds for >99.99% kill rates against multi-drug-resistant strains) that the organisms have no opportunity to develop resistance. Switch the light off and the reaction stops. There is no antibiotic, no systemic exposure, no compliance issue.

That last point matters more than it might sound. The current standard of care in nasal decolonisation is mupirocin, a topical antibiotic that requires twice-daily self-application for five days before surgery. Real-world compliance is poor — typically 30–40% — and resistance rates are climbing. Steriwave is a single, nurse-administered treatment with effectively 100% compliance. That is not a marginal product improvement; in clinical workflow terms, it is a different category.

Three layers to the business

Steriwave (the cash-generative core). The lead product, marketed under the Steriwave® brand outside the US. Already CE-marked in Europe and approved in Canada, Australia, Mexico and several other countries. Deployed across NHS Trusts (Mid Yorkshire, Leeds, King’s College), all five British Columbia Health Authorities, the Mater Hospital in Sydney, ENT specialist centres in Madrid, and listed with NHS Supply Chain — recently classified as an “Innovation Product”.

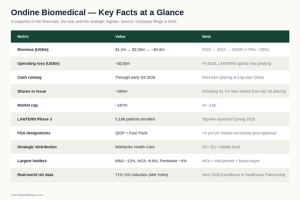

The US opportunity (LANTERN). Photodisinfection is investigational in the US, with FDA Fast Track and Qualified Infectious Disease Product (QIDP) designations in hand. The Phase 3 LANTERN trial — 5,188 patients across 14 HCA Healthcare hospitals and four Canadian centres — completed enrolment on 13 April 2026, with top-line data guided for Spring 2026. A positive readout opens up the $35bn US healthcare-associated infection burden in a category with no FDA-approved product specifically indicated for SSI prevention.

The pipeline. Photodisinfection is a platform. Beyond nasal decolonisation, Ondine has investigational programmes in chronic rhinosinusitis, ventilator-associated pneumonia (disinfection of endotracheal tubes), burns and chronic wounds, catheter-associated UTIs, and topical antiviral treatments for the upper respiratory tract. None of this is in my numbers — but it is genuine optionality if LANTERN validates the platform.

The UK base: validation, with caveats

The UK and Canada operations do two useful things and one less useful one. Worth being honest about both.

What is working is the data. Real-world evidence is accumulating that supports the clinical and economic case for the technology:

- Real-world clinical proof. The Mid Yorkshire NHS Trust deployment in orthopaedic surgery delivered a 71% reduction in surgical site infections in hip surgery and zero observed SSIs in the knee cohort over the evaluation period. Real-world data, in routine NHS workflow, broadly consistent with the historical clinical evidence base.

- Independent health economics. A York Health Economics Consortium analysis quantified savings of £1.49 to £2.38 per £1 spent on Steriwave across major surgical specialities, rising to £3.92 per £1 in cardiac, with a UK-wide opportunity of up to £200m in annual NHS savings.

- Institutional recognition. Won the 2026 Excellence in Healthcare Partnership Award; shortlisted for the HSJ Partnership Awards; classified as an “Innovation Product” by NHS Supply Chain — credibility that lowers procurement friction inside the NHS.

What has been less useful is the commercial pull. The Mölnlycke Health Care distribution partnership signed in September 2024 was a meaningful credibility signal — Mölnlycke is a tier-one Swedish MedTech major and they do not put their name on speculative products. But in practice the rollout has been gradual rather than aggressive. Adoption is still happening one trust at a time, and there is not yet a flagship multi-trust framework win that would shift UK revenue from “expanding pilots” to “embedded standard of care”.

I treat the UK as latent value rather than the active engine of the thesis. The data is real and 2025 unaudited revenue still grew +29% off a small base — but anyone underwriting Ondine on the basis of UK rollout pace alone is going to be disappointed. The active engine is the US.

HCA Healthcare: the real story

The piece of the Ondine story I think the market is genuinely under-pricing is not the UK rollout. It is the strategic alignment with HCA Healthcare on the US side.

In January 2025, HCA Healthcare — one of the largest private hospital groups in the US, with ~182 hospitals and ~2,300 ambulatory sites of care — invested US$4m in Ondine via its hInsight-NX subsidiary, taking ~8.6% of the enlarged share capital at 10.5 cents per share. That makes HCA Ondine’s second-largest shareholder after M&G.

That stake is meaningful for three reasons that compound on each other:

- HCA is the LANTERN trial partner. All 14 US trial sites are HCA hospitals, which means HCA has unrivalled internal visibility into how Steriwave is performing in real surgical workflows long before any external party sees the data.

- HCA is the intended primary US commercial channel. Management has been explicit that the post-approval launch strategy will lead with the HCA network. Even modest penetration across 182 hospitals translates into a very different revenue trajectory than a typical small-cap medtech rollout.

- HCA is now an aligned equity holder. The cheque, sized at ~8.6% of the company at the prevailing price, sits alongside the trial collaboration. A trial partner that also writes a cheque is a very different kind of validation than a trial partner alone — particularly one that has unrivalled internal data on what works in their own hospitals.

I do not think it is a coincidence that the institution with the best ground-truth view of the technology has chosen to express that view in equity. Combine that with LANTERN being run inside the HCA network, and you have a setup where the trial outcome and the commercial outcome are tightly linked: a positive readout means HCA — already an investor — has the playbook to roll Steriwave across its 182 hospitals as fast as procurement and reimbursement allow. That is the upside you do not get by underwriting the UK alone.

LANTERN: the catalyst

That said, the share price will be set by LANTERN. So let’s be clear about what we’re waiting for.

LANTERN (Light-Activated Antimicrobial Nasal Therapy to Prevent Surgical Site Infections) is a group-randomised crossover Phase 3 study. 5,188 patients, 14 HCA Healthcare hospitals in the US, four major Canadian centres, comparing standard infection prevention practice with and without Steriwave. The primary endpoint is the reduction in adjudicated SSIs.

Three things stand out about the design. First, the size: 5,188 patients is large enough to detect even modest treatment effects with statistical power. Second, the crossover design controls for hospital-level confounders by comparing each site against itself. Third, the endpoint is a hard clinical outcome — SSIs adjudicated by an independent committee — not a surrogate marker.

As of the March 2026 update, ~80% of monitoring visits were complete and ~80% of primary endpoint adjudications done. Data integrity numbers are clean (>92% CRF completion, >98% participant retention). Top-line is guided to Spring 2026 — so we are weeks to a few months out at the time of writing.

If LANTERN delivers anything close to the real-world Mid Yorks numbers, Ondine has the basis for an FDA submission in a category with no incumbent approved product. Pre-NDA meeting is guided for early Q4 2026. That is when the market starts pricing in genuine US commercial optionality.

The FDA designations are quietly valuable

One thing routinely under-appreciated in Ondine write-ups is the optionality embedded in the regulatory designations themselves. Steriwave has two:

- Qualified Infectious Disease Product (QIDP). Granted in 2018 under the GAIN Act. The headline benefit is five additional years of US market exclusivity post-approval, on top of any patent protection, plus Priority Review at NDA stage and the full benefits of Fast Track. In a category with no incumbent FDA-approved product, that exclusivity period is genuinely valuable — it materially extends the cash-flow window for any successful launch.

- Fast Track designation. Granted in 2019. Speeds up FDA interactions and supports more frequent meetings, which lowers execution risk on the regulatory pathway itself.

Combined, these designations mean that a positive LANTERN read-out followed by approval would give Ondine a regulatory moat in nasal decolonisation that no competitor could replicate without their own pivotal trial — and even then, would have to wait out the QIDP exclusivity window. The market is treating FDA approval as a binary event; what it should also be valuing is the de-facto monopoly window on the other side of it.

Financial shape: thin, but not panicking

Let’s not pretend this is a fortress balance sheet.

Revenue and growth. 2024 revenue was $2.05m, up 70% year-on-year off a small base, with 2025 unaudited revenue up another ~29%. Full-year 2025 results are now guided for early June 2026. The absolute numbers are tiny relative to the addressable market, but the growth and the year-on-year acceleration in account utilisation are encouraging.

Losses and burn. 2024 loss of around $19m, ~32% wider than the prior year. The widening reflects ramped LANTERN trial spend and commercial preparation; it is not operating-cost rot. With LANTERN now fully enrolled and commercial-scale manufacturing being brought in-house, I would expect the cost trajectory to bend post-data.

Cash and the recent placing. In April 2026, Ondine raised £5m at 12p — roughly 10% of market cap — at just a 4% discount to the prior close. That is worth dwelling on. AIM fundraising in 2026 has been ugly: deeply discounted dilutive raises and broken share registers are the norm. Ondine pulled off a meaningfully sized placing at near-zero discount, with director participation alongside US investors, in that environment. That is the market voting on the quality of the LANTERN setup with real money. Net proceeds extend the cash runway through early Q4 2026 — explicitly enough to cover the LANTERN study report, GMP commercial-scale production batches, stability work, and the Pre-NDA meeting. The runway is deliberately tight: management is running it close because raising at higher prices post-data, if positive, is far less dilutive than raising more now.

Shareholder register. M&G holds ~13% (recently increased from ~9%); HCA Healthcare’s hInsight-NX subsidiary holds ~8.6% (from the January 2025 strategic investment); Pentwater Capital ~4%. The combined institutional ownership is the kind of register one would expect to support a follow-on financing if needed.

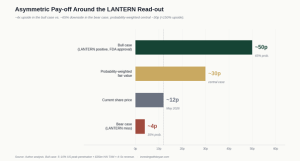

Valuation

Pricing a pre-FDA, loss-making single-product story is by definition more scenario-driven than my MTI-style sum-of-the-parts. Here is how I think about it:

Bull case (LANTERN positive, FDA approval ~2027–28). US TAM of ~$35bn HAI burden and ~12m relevant annual surgeries. Even modest peak penetration of 5–10% at a treatment ASP consistent with the YHEC pricing implies $60–150m of US revenue at maturity, on top of a UK/EU/Canada base growing into the $20–30m range via Mölnlycke. Apply a 4–5x revenue multiple — defensible for a profitable medtech with a moat — and the equity is worth 40–60p per share post-likely-dilution. Call it 50p central. The QIDP exclusivity meaningfully extends the window over which those cash flows are protected.

Bear case (LANTERN miss or borderline result). US optionality essentially disappears; the company reverts to a UK/EU/Canada commercial business worth, optimistically, 2–3x near-term revenue, plus the unavoidable cost of further dilutive funding. 3–5p central, say 4p.

Probability weights. Phase 3 success rates across pharma sit around 60–65%. For programmes with strong Phase 2 / real-world supporting data (which Ondine has), the historical hit rate is closer to 70–75%. I will use 65% / 35% to be conservative.

That gets me to 0.65 × 50p + 0.35 × 4p ≈ 34p, which I round down to ~30p for further haircuts (incremental dilution beyond the recent placing, FDA timing slippage, commercial ramp risk). Even at that conservative round-down, today’s ~12p offers ~150% upside on the central case, with the binary skew giving you ~4x in the good case and ~65% downside in the bad.

That is the kind of risk/reward that justifies a meaningful but disciplined position — meaningful because the central-case asymmetry is genuine, disciplined because the bear case is genuine too.

Key risks

I’d be misleading anyone if I left these out:

- LANTERN is binary. A primary endpoint miss is not survivable for the equity in its current form. Even a marginal positive (statistical significance with a clinically modest effect size) could disappoint relative to the real-world Mid Yorks numbers and pressure the multiple.

- Cash runway is tight. Through early Q4 2026 only. If LANTERN data slips or the read is mixed, the next raise will be larger and more dilutive. The recent placing at 12p is a baseline, not a floor.

- FDA pathway risk. Even with positive data, the submission, review and any post-marketing requirements add 12–18 months of uncertainty. Reimbursement coding in the US is also a non-trivial step.

- Commercial ramp outside the US is real but slow. NHS adoption, despite excellent unit economics, has been gradual. Most rollouts have been one trust at a time. Mölnlycke is doing the right work, but converting NHS trial deployments into recurring procurement is a multi-quarter exercise.

- Concentration on a single product. The pipeline is genuine optionality, but everything material in the model is Steriwave for nasal decolonisation. Other indications would need their own trials and approvals before they contribute to revenue.

- AIM small-cap liquidity. Sub-£70m market cap, with an inherently volatile shareholder base around binary catalysts. Position-sizing matters more here than in nearly anything else in the portfolio.

What I’m watching from here

The next six to nine months will be defined by the LANTERN data. Three things I want to see:

- LANTERN top-line shows a clear, clinically meaningful reduction in SSIs — ideally double-digit relative reduction in the primary endpoint, broadly consistent with the real-world signal already on the ground.

- 2025 full-year results (early June 2026) confirm the +29% unaudited growth translates into a comparable revenue figure, with improving gross margins as in-house manufacturing kicks in.

- NHS conversion — one or two sizeable multi-trust framework wins through Mölnlycke that move UK revenue from “expanding pilots” to “embedded standard of care” in defined surgical pathways.

If LANTERN delivers and the commercial story holds, this becomes a very different conversation — and I will look to add on the data, not before. If LANTERN disappoints, the question becomes whether the rump UK/EU business is worth the smaller-cap valuation that follows; the position is sized so that I can hold it through that without forced selling.

This is, in short, a genuinely asymmetric bet at the current price — and one I am happy to be running as a conviction holding into the data.

Disclosure: I hold a position in Ondine Biomedical at the time of writing. This is not investment advice — always do your own research. Read the full disclaimer at investingwithboyan.com.

If you found this useful, more analysis is available at investingwithboyan.com — or subscribe via the form in the sidebar to get new pieces straight to your inbox.