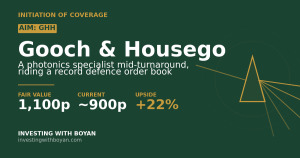

Gooch & Housego (AIM: GHH) — Initiation of Coverage

The Quick Take

- Company: Gooch & Housego (AIM: GHH) — UK-headquartered specialist manufacturer of photonics components and systems, serving Aerospace & Defence, Industrial and Life Sciences end-markets

- Thesis: A 77-year-old precision photonics business midway through an operational turnaround — adjusted operating margins moving from 7.7% to 9.6% and targeting mid-teens by 2028 — with a structural defence tailwind that has just delivered a record order book and a US acquisition that opens the largest A&D market in the world

- Catalyst: Order book +16.5% to a record £167.3m at H1 FY26, semiconductor cycle now turning, and the Global Photonics integration unlocking US defence contracts that the UK parent simply could not pursue alone

- Valuation: ~900p vs my fair value of 1,100p (≈22% upside) — the operational recovery is increasingly visible in the order book and the medium-term margin journey to mid-teens is now both credible and progressing, justifying a 22-23x forward P/E for a recovering specialist photonics business with structural defence exposure

- Key risk: The shares have already more than doubled from 378p in the past year. Industrial laser and semiconductor end-markets are recovering not recovered — any wobble in that recovery hits the margin trajectory directly

- Position: Built progressively over the past six months at a blended ~590p; smaller position in the portfolio, reflecting both the AIM small-cap volatility profile and the fact that the asymmetric setup has narrowed

- Time horizon: 2–3 years to the mid-teens margin target; 3–5 years to fully credit the strategic repositioning

This is a different kind of write-up to my MS International or Ondine pieces, both of which were initiations into businesses I thought were structurally mispriced. G&H sits between the two ends of the spectrum — a high-quality compounder that has already had a strong run, but where the recent operational delivery (record order book, A&D acceleration, semiconductor recovery starting) genuinely strengthens the medium-term thesis rather than just confirming it. For those of you carefully reading my posts, I mentioned my purchase back in January, when the shares were still trading at around 620p. Unfortunately I didn’t get a chance to do the write up there and then, so here we go. The shares went from 378p to a fresh high of 918p in twelve months, which means anyone reading this who hasn’t already built a position is paying for the early-stage recovery — but the path from here to mid-teens margins is now clearer than it was six months ago, and 22% upside on my central case feels defensible.

What Gooch & Housego actually does

G&H is a specialist manufacturer of photonic components and systems. In plainer English: the business makes the precision optical components — lenses, mirrors, crystals, fibre-optic assemblies, electro-optic modulators, acousto-optic devices — that go inside lasers, imaging systems, semiconductor lithography tools, fibre-optic data networks, military targeting systems, medical instruments, and the various pieces of scientific apparatus that need to manipulate light with extreme precision.

The business was founded in 1948 in Ilminster, Somerset, by Archibald Gooch and Albert Housego, originally as a crystal-growth and precision optics specialist. Over the subsequent decades it grew through a long series of acquisitions of “best-in-breed” specialists in adjacent optical technologies, becoming the consolidator of choice for niche photonics businesses across the UK and US. Today it employs around 975 people, operates manufacturing sites across the UK, USA and Continental Europe, and generates £150m+ of revenue at a roughly 10% operating margin.

The business model is more attractive than the contract-manufacturing label might suggest. G&H’s products are typically designed into customer platforms — a specific laser, a specific defence vision system, a specific lithography tool — over multi-year qualification cycles. Once designed-in, the parts are very difficult to replace because the customer would have to re-qualify the entire system. That creates a recurring revenue base with high gross margins (30%+) for the qualified products, supplemented by ongoing engineering services for next-generation designs. The capital intensity is reasonable, returns on capital are improving as the margin story plays out, and the technical moat — knowing how to grow crystals that maintain optical purity at scale, knowing how to polish surfaces to single-digit nanometre tolerance, knowing how to package fibre-optic assemblies for harsh environments — is genuinely deep.

The three segments

G&H reports across three end-market segments, and the segment mix is where the recent story has been most interesting.

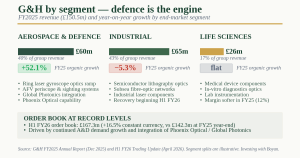

Aerospace & Defence. The growth engine of the recent past and the most interesting part of the equity story today. Revenue grew 52.1% in FY25 (year to September 2025), driven by higher production of super-polished optical components for ring laser gyroscopes (used in inertial navigation systems for missiles, aircraft and naval platforms), the ramp of periscope and sighting systems for armoured fighting vehicles, and the integration of two acquisitions (Phoenix Optical and Global Photonics) that materially expanded the A&D capability. The H1 FY26 update confirmed continued strong growth in this segment and a record order book underpinned by both new and existing defence customers. Crucially, the May 2025 acquisition of Global Photonics — a US-based optical systems specialist — establishes a US optical systems engineering and manufacturing hub that lets G&H pursue US Department of Defense work it simply could not access from the UK. The strategic logic is to replicate the UK optical systems hub in the US, and given that the US accounts for roughly half of global defence spending, this is a meaningful expansion of the addressable market.

Industrial. The segment that has been the drag on group performance for the past two years. Industrial covers fibre-optic components for advanced semiconductor lithography (a major customer is ASML’s deep-ultraviolet and EUV ecosystem), telecom-grade fibre optics for subsea data networks, and components for industrial lasers used in semiconductor and microelectronics manufacturing. The segment declined 5.3% in FY25 as semiconductor and industrial-laser customers worked through inventory and capex cycles. The H1 FY26 trading update was the first clear signal that this cycle is turning — semiconductor recovery is now described as “encouraging” rather than “anticipated,” and industrial laser markets are improving alongside it. Given that this segment has historically been the largest revenue contributor and is structurally exposed to the AI-driven semiconductor build-out, a sustained recovery here is materially positive for both group revenue and group margins (Industrial margins are typically the highest in the group).

Life Sciences / Biophotonics. The most under-the-radar segment, serving medical device manufacturers, in-vitro diagnostics companies and laboratory instrument makers with specialty photonic components and complete systems. Revenue was broadly flat in FY25 and Life Sciences operating margins actually softened to 12.0% (from 14.7%) — partly mix, partly the absorption of investment in new product development. This segment is smaller than the other two but offers genuine optionality as G&H’s complete-system capability matures and the company can sell finished medical instruments rather than just components inside other people’s systems.

The defence acceleration: from optics shop to systems supplier

The single most important narrative shift at G&H over the past two years is the transition from selling optical components to selling complete optical systems for defence applications.

The traditional G&H business was a components vendor. The customer was the prime contractor — a Lockheed, a Raytheon, a BAE — and G&H supplied the precision optical sub-assembly that went inside the prime’s larger system. Margins on this work are decent but the value-add is bounded by being a tier-2 supplier, and the customer relationship is mediated through procurement rather than engineering.

The strategic pivot has been to move up the value chain into complete systems — periscope and sighting systems for armoured fighting vehicles, integrated vision systems for naval platforms, complete sub-assemblies for inertial navigation. These products are sold directly to defence ministries or via lighter prime relationships where G&H owns the design responsibility. Margins are higher, customer relationships are deeper, and the qualification cycles are longer — but the resulting revenue base is far stickier.

Three things have accelerated this transition recently:

- The Phoenix Optical acquisition (October 2024, £6.75m) added complementary precision optics capability and the customer relationships to deploy it across defence applications. Phoenix’s super-polishing capability is now feeding the ring laser gyroscope ramp directly.

- The Global Photonics acquisition (May 2025, $17.5m) is the more strategically consequential move. Global Photonics is a US-based optical systems specialist with existing US Department of Defense customer relationships and ITAR-cleared manufacturing capability. This is what unlocks the US market — without a US optical systems engineering hub, you cannot meaningfully pursue US DoD contracts. With it, you can. The combined Global Photonics + Phoenix Optical capability has already secured new defence orders across the US, UK and Europe and is expanding capacity in line with planned capex.

- The structural defence spending environment. NATO countries are increasing defence budgets, the US DoD is funding programme acceleration for sensor and targeting modernisation, and the Ukraine conflict has demonstrated the importance of advanced optronics in modern warfare. None of this directly translates into G&H orders, but it shifts the procurement environment in favour of suppliers who can deliver complex optical systems on accelerated timelines.

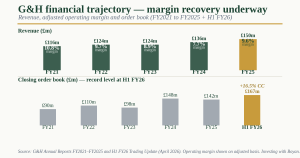

The recent order book number — £167.3m at H1 FY26, up 16.5% on constant-currency basis — is the visible manifestation of this transition. The order book is now larger than full-year revenue, which gives meaningful FY26 and into-FY27 visibility, and the mix is increasingly weighted to the A&D systems work that supports the margin story.

Financial shape: the margin journey is the story

The financial picture is genuinely improving, but the operational turnaround has further to run.

Revenue. FY25 (year to September 2025) revenue was £150.5m, up 10.7% on the prior year and 5.6% on an organic constant-currency basis. The H1 FY26 print of £81.9m (+9.1% organic CC) suggests full-year FY26 revenue in the £160-170m range, with the second half typically slightly stronger.

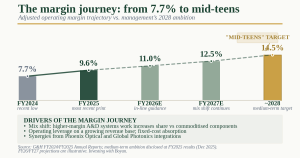

Operating margins. This is the part that matters. FY24 adjusted operating margin was 7.7%. FY25 stepped up to 9.6%. The medium-term target is “mid-teens” — let’s call it 14-15% — by 2028. That’s a 5+ percentage-point margin expansion journey over three years, which on £170m+ of revenue translates to approximately £8-10m of incremental operating profit just from the margin uplift, on top of any revenue growth. The drivers are a mix of operational leverage (fixed-cost absorption as revenue grows), mix shift (higher-margin A&D systems work vs lower-margin industrial components), productivity initiatives, and integration synergies from the recent acquisitions.

Adjusted earnings. FY25 adjusted PBT was £11.9m (vs £8.1m) and adjusted diluted EPS was 34.6p (vs 25.1p). The statutory figures are materially lower — PBT £5.3m, EPS 13.3p — reflecting amortisation of acquired intangibles and one-off charges related to acquisitions and restructuring. The adjusted numbers are the right ones to focus on for the long-run earnings power, but the gap between adjusted and statutory is real and worth understanding.

Balance sheet. Net debt was £37.0m at 31 March 2026 (H1 FY26), with £15.7m of additional headroom on the revolving credit facility. This is a meaningful step up in leverage from the historically low-debt G&H balance sheet, reflecting the Global Photonics acquisition and capacity expansion capex. Net debt / EBITDA is around 1.4x on the run-rate — not stretched, but worth monitoring as the integration costs flow through.

Cash conversion. Working capital has been an investment headwind during the order book build (more inventory and WIP to service the growing pipeline) and capex has been elevated to support capacity at the acquired businesses. As the order book converts to revenue and capacity comes online, cash conversion should normalise back toward 80%+ of operating profit through FY27.

Valuation: priced for the margin journey to deliver

At ~900p, G&H’s market capitalisation is approximately £246m on roughly 27.4m shares outstanding.

On FY25 adjusted EPS of 34.6p, the trailing P/E is around 26x. That sounds expensive for an AIM small-cap. On FY26E adjusted EPS — which my estimate puts at 40-45p reflecting revenue growth and continued margin progression — the forward P/E is closer to 20-22x. Still optically expensive, but bear in mind that this is a business with 30%+ gross margins, a credible path to mid-teens operating margins, structural defence exposure, and a record order book providing visibility.

The relevant comparables — Avon Protection, QinetiQ, Cohort — trade in the 12-25x forward P/E range depending on their growth and margin profile. G&H sits at the upper end of this range, justified by the highest organic growth rate in the group and the genuine optionality on the margin expansion.

My fair-value framework:

- Bull case (~1,200-1,400p, 33-56% upside). Mid-teens margins achieved on track by 2028 (or earlier if A&D mix accelerates). FY27E EPS reaches 55-60p as revenue grows toward £180m and margins step to 13-14%. Multiple sustained at 22-24x forward earnings on the visible growth and margin trajectory. US defence wins materialise meaningfully through Global Photonics. Order book continues to compound.

- Base case (~1,000-1,200p, 11-33% upside). Margin progression continues but the full mid-teens target slips to 2029 or beyond. FY27E EPS reaches 50p. Multiple holds at 19-22x. A&D growth normalises to 15-20% from the FY25 surge. Industrial recovery delivers as expected, neither faster nor slower.

- Bear case (~650-800p, 11-28% downside). Industrial recovery stalls. Margin expansion plateaus at 10-11%. Multiple compresses to 14-16x on stalled earnings progression. AIM-small-cap risk-off compounds the de-rating. Tariff impacts on raw materials prove more persistent than current management commentary suggests.

Probability-weighting (35% bull / 50% base / 15% bear) gives a central fair value of approximately 1,100p on a 12-18 month view — roughly 22% upside from current levels. The probability tilt toward the bull case reflects the genuine strength of the H1 FY26 trading update: a record order book up 16.5% on constant currency, A&D demand continuing to accelerate, semiconductor recovery now described in management commentary as “encouraging” rather than “anticipated,” and the Phoenix Optical / Global Photonics integrations progressing on plan. The fundamental case has strengthened materially over the past six months, and a 35/50/15 distribution reflects that better than the 30/50/20 a prudent analyst would have applied twelve months ago.

I should be honest about what this valuation framework implies. The bull case still requires the medium-term margin journey to be substantially delivered earlier than the 2028 target, but the H1 trading update materially de-risks that path. The base case is what management is currently guiding to, with double-digit upside even in that scenario. The bear case is what happens if either the operational story stalls or the AIM-small-cap multiple compresses, and the downside is meaningful — but the probability is lower today than it was twelve months ago. The risk-reward at 22% central upside with a credible bull case offering 33-56% is genuinely attractive, even after the shares have already more than doubled from 378p.

The capital-return profile is also worth noting. G&H pays a modest dividend (around 13-14p, ~1.5% yield) and does not run a buyback programme. Most of the cash flow is currently funding capacity expansion and integration capex. Total shareholder return is therefore overwhelmingly driven by the share price, which means the margin journey delivering — or not — is everything.

Key risks

- The shares have already re-rated meaningfully. From 378p to 918p in twelve months is a 2.4x move. While my central case still implies 22% upside from here, the easy entry-level multiple expansion is behind us. The remaining upside depends on operational delivery — a small wobble in execution would be punished by the multiple.

- Industrial recovery is recovering, not recovered. The semiconductor and industrial laser cycle is notoriously volatile. The H1 FY26 commentary was “encouraging signs” of recovery, not “recovery confirmed.” If end-market demand softens again, this segment becomes a drag.

- Margin journey is multi-year and incremental. “Mid-teens by 2028” is the medium-term target, not a near-term reality. The trajectory from 9.6% to 14-15% requires consistent execution across mix shift, productivity and acquisition integration over three years. Plenty can go wrong.

- Tariff and trade policy exposure. G&H sources specialty optical raw materials globally and ships product internationally. Retaliatory tariffs on key inputs have been a real headwind through 2025-26 and may continue. Management has been managing this proactively but it remains a margin risk.

- AIM small-cap profile. £246m market cap, AIM-listed, modest free float, single-digit-million daily volumes. Liquidity matters when you want to exit, and AIM-IHT-related selling can create technical pressure regardless of fundamentals.

- Customer concentration. G&H discloses limited customer detail but a meaningful proportion of revenue comes from a small number of large customers across the three segments. Any single customer souring or in-housing production has a disproportionate impact on segment results.

- Acquisition integration. Phoenix and Global Photonics are being integrated concurrently. Both are progressing as planned per the H1 update, but acquisition integration is rarely without friction and the capacity expansion is ongoing.

- Statutory vs adjusted earnings gap. The persistent and meaningful gap between adjusted and statutory profits is a yellow flag worth monitoring. As acquired intangibles roll off the amortisation schedule the gap will narrow, but the trajectory of statutory earnings is what eventually matters for cash returns to shareholders.

Three concrete operational tests will define the next 12 months:

- Interim results on 2 June 2026 confirm the H1 trading update at the underlying margin and cash level. The trading update gave the top-line and order book but the operating leverage at the H1 print is the proof point.

- Industrial / semiconductor recovery sustains through H2 FY26 and into FY27. Watch the commentary on fibre optic component volumes in subsea data networks, advanced lithography ramp volumes, and industrial laser end-market commentary — these are the leading indicators of group margin upside.

- The first material US defence contract wins through the Global Photonics platform. The acquisition rationale was access to the US DoD market, and within 12-18 months the order book should be visibly reflecting that with first-tranche programme wins.

If those three boxes tick, this becomes a different conversation — the multiple should sustain in the upper bull-case range and the margin trajectory delivers cleanly. If industrial recovery stalls and the A&D order momentum normalises before US wins materialise, the share price gives back a meaningful chunk of the recent gains. The position is sized appropriately for either outcome — meaningful but not central to the portfolio.

In summary, Gooch & Housego is a genuinely high-quality precision photonics business that is delivering on the operational turnaround thesis with growing visibility. The order book is at a record, defence growth is accelerating, the US expansion is strategically right, and the margin journey toward mid-teens is real and increasingly de-risked by the operational delivery. The shares have more than doubled in twelve months, but the H1 FY26 trading update materially strengthens the medium-term case rather than just validating it — and the 22% upside to my central fair value still leaves room for the equity to reward patient holders through the 2-3 year margin progression. The AIM-small-cap profile means the shares will be more volatile than the underlying business performance, so position sizing matters. For me, this fits a smaller portfolio slot with meaningful optionality, and I’m happy to keep adding measuredly on weakness while letting the medium-term thesis play out.

Disclosure: I hold a position in Gooch & Housego at the time of writing, acquired progressively over the past six months at a blended price of approximately 590p. This is not investment advice — always do your own research. Read the full disclaimer at investingwithboyan.com.

If you found this useful, more analysis is available at investingwithboyan.com — or subscribe via the form in the sidebar to get new pieces straight to your inbox.