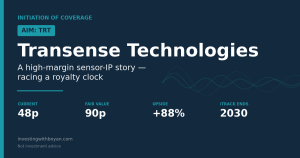

Transense Technologies (AIM: TRT) — Initiation of Coverage

The Quick Take

- Company: Transense Technologies (AIM: TRT) — Oxfordshire sensor-technology group with three income streams: SAWsense, Translogik and a Bridgestone royalty.

- Thesis: A high-margin, IP-rich micro-cap whose profits today come almost entirely from a royalty that expires in 2030. The whole case is whether SAWsense scales fast enough to replace it — cheap if it does, a melting ice cube if it doesn’t.

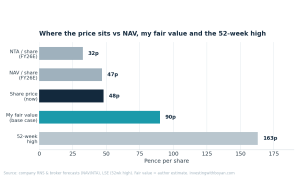

- Valuation: 48p vs my fair value of 90p (≈88% upside). Wide cone: ~40p bear, 180p+ bull.

- Rating: Speculative Buy (high risk)

- Key risk: The ~£2m iTrack royalty is ~100% margin and ~43% of revenue. Strip it out and the core divisions lose ~£2m a year. The licence ends in 2030.

- Position: Former holder (in ~80p, out ~120p into the Sept-25 warning). Revisiting as a speculative special situation (added at 0.5% of my portfolio)

- Time horizon: 3–5 years (this is a 2027/28 production story).

Why I’m looking at this again

I owned Transense once before — in at roughly 80p, out at about 120p when I read the September 2025 finals as a soft warning and the operational-gearing story started slipping to the right. I bought into the story back in the day because at the time the company was profitable and the entire market cap was underwritten by the royalties from iTrack(see later). Since then the company has hired a new CEO(managing director) and has invested in anticipation of scaling up. Unfortunately, this was slower than the management expected and at that point I decided to sell. The shares are now 48p, down roughly 70% over the past year and sitting close to their 52-week low (range ~47–163p), capitalising the whole business at just ~£7.3m. A 22 June trading update trimmed FY26 and moderated FY27 again, so on the face of it nothing has improved.

But two things made me reopen the file. First, the de-rating has been brutal enough that the quality of the underlying assets — patent-protected sensor IP, genuinely blue-chip customers, a cash-generative royalty — is arguably no longer in the price. Second, at the 23 June Investor Meet Company session the Chairman was unusually explicit: guidance has been deliberately rebased to what is “highly likely” rather than the full pipeline, and the Board expects to announce commercial wins shortly. If that’s right, the risk/reward looks very different from where the tape is trading. In addition, I respect the leadership team of the company and they come across as honest bunch with skin in the game.

This note lays out the business, the financials behind the FY26 reset, my valuation, and — importantly — the things that would stop me from buying.

What Transense actually is

Three quite different income streams sit under one tiny listed shell:

- SAWsense — the growth engine. Designs, supplies and licences sensors built on patent-protected Surface Acoustic Wave (SAW) technology, which measures torque, force, pressure and temperature without contact and without a battery in brutal environments. Target markets: aerospace, electric motors & drives, off-highway and industrial machinery, robotics and motorsport. Customers named by the company include GE Aerospace, Airbus, Parker Meggitt and McLaren Applied, plus several unnamed Tier-1s.

- Translogik — connected commercial-vehicle tyre-inspection tools (the TLGX range) sold to tyre majors, fleets and service centres, increasingly with a software/data layer.

- Bridgestone iTrack royalty — residual, near-100%-margin royalty income from an off-highway tyre-monitoring system Translogik built and sold to Bridgestone in 2020. The IP is licensed exclusively to Bridgestone under a ten-year deal expiring in 2030.

The single most important thing to understand about Transense is the relationship between these three: iTrack is the profit; SAWsense and Translogik are, for now, the investment (especially SAW for the bullcase). Hold that thought.

SAWsense — the reason to own it

This is where the optionality lives. SAW sensing solves a real engineering problem: how do you measure torque or temperature on a spinning shaft, a motor rotor or a jet-engine component where you can’t run wires or batteries? SAW devices are passive and wireless, interrogated remotely — which is why they keep turning up in the hardest applications.

The customer list is the headline. The flagship is the GE Aerospace T901 programme (the engine destined for the US Army’s Black Hawk and Apache fleets), which is already generating revenue. Around it sits a development pipeline spanning aerospace, automotive eDrive, aircraft landing gear, motorsport, and — the one that gets people excited — robotics, where torque sensing in actuator joints is a natural fit for the humanoid/industrial wave.

Operationally, the pilot production line is now largely complete, with individual stations in place. That matters more than it sounds: the whole bottleneck for a business like this is the leap from “feasibility study” to “qualified, repeatable volume production.” Management has the line; now it needs the orders.

One important quality check on the SAW numbers, though: a meaningful slice of SAWsense revenue is grant income, not commercial sales. The automotive eDrive work (the ~£11m Protean PULSE in-wheel-motor consortium) and the aircraft landing-gear programme are grant-funded collaborative R&D. That funding is genuinely useful — it’s non-dilutive, de-risks the engineering and validates the technology alongside serious partners — but it is lumpy, time-limited and not the same as a customer paying for product. So the underlying commercial SAW run-rate is lower than the ~£1.3m headline, and the bar for what counts as real “conversion” is higher than the top line implies.

And there’s the rub. SAWsense revenue is growing (FY26E ≥£1.3m vs £1.12m in FY25), but the pace of commercial conversion keeps disappointing. Customers are slow to commit from initial feasibility work to larger, paid non-recurring-engineering (NRE) contracts. Earliest production dates are 2027/28. So this is a real business with real customers — but it’s a “show me” story measured in years, not quarters.

Translogik — quietly re-mixing

Translogik is the least glamorous leg and is, in revenue terms, slightly down year-on-year (FY26E ≥£1.25m vs £1.32m). The story underneath is more interesting than the headline: demand from the global tyre majors softened, but the company is offsetting that with traction among smaller customers, distribution partners and a building SaaS/data layer that should lift the quality and recurrence of the revenue mix over time. Regulatory drivers around tyre safety and compliance remain a structural tailwind.

It’s not the reason to own the stock, but it’s a credible second growth vector with better-quality revenue if the SaaS mix builds, and new product launches are slated to come on stream in FY27.

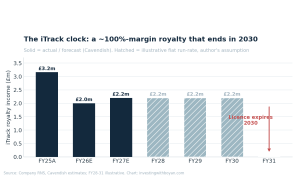

iTrack — the cash engine, and the clock

Now the uncomfortable part. The iTrack royalty is forecast at ~£2.0m in FY26, growing modestly thereafter. Because it carries virtually no cost, it drops almost entirely to profit. It is the thing that lets Transense fund two loss-making divisions without diluting shareholders.

It is also finite. The licence runs out in 2030.

The iTrack royalty is the profit engine — and it has a defined end date. FY28–31 shown illustratively.

That single fact reframes the entire investment. You are not buying a perpetual royalty plus a growth option. You are buying roughly four more years of high-margin royalty cash, during which SAWsense (and Translogik) must reach self-sustaining profitability — otherwise what’s left in 2030 is two divisions that, today, lose money. The clock is the thesis.

The FY26 reset, explained

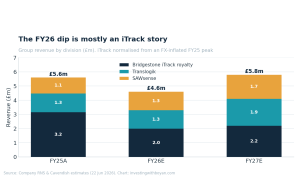

The market reads “profit collapse” and panics. The honest reading is more nuanced — and you only get it by splitting the revenue.

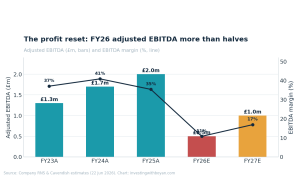

The FY26 dip is mostly an iTrack story(which was know years in advance as but the market somehow got surprised). This was all due to contractual reduction in the royalty income which was baked in at the inception. iTrack ran at roughly £3.2m in FY25 — an FX-inflated, cyclically strong year — and has normalised to ~£2.0m in FY26. That’s a ~£1.2m swing in a near-100%-margin line, which on its own explains the bulk of the EBITDA drop below. Add a step-up in operating costs (headcount roughly doubled to ~30 in 2024 to build out engineering and commercial capability) and softer Translogik, and you get this:

Adjusted EBITDA more than halves, from £2.0m (FY25) to ~£0.5m (FY26E), with margin compressing from the mid-30s to ~11%. Forecasts pencil a partial recovery to ~£1.0m in FY27E as iTrack stabilises and SAWsense builds.

So FY26 isn’t a demand catastrophe so much as an FX/cyclical air-pocket in iTrack colliding with a planned investment build. That’s more forgivable. But it leads straight to the chart that should anchor your thinking:

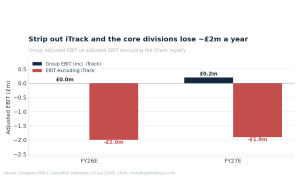

Strip out iTrack and the core divisions lose ~£2m a year, at both FY26E and FY27E. Group adjusted EBIT is barely positive only because the royalty is carrying it. Until that ex-iTrack line turns, Transense is a royalty in run-off subsidising a venture-stage sensor business. The bull case is that SAWsense’s operational gearing flips that line decisively before 2030; the bear case is that it doesn’t, and the royalty rolls off into a loss-making rump.

Balance sheet & cash — thin, and tightening

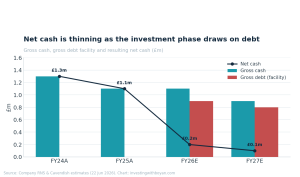

This is the risk people underweight. Net cash has fallen from £1.1m (FY25) to a forecast ~£0.2m (FY26E), and the company is now drawing a £900k debt facility, expected fully drawn by year-end.

Free cash flow is negative through the investment phase (roughly -£1.0m modelled for FY26E), capex runs ~£0.8–0.9m a year, and working capital is stretched (receivables out to ~167 days on the FY26E model). Management’s stated strategy is to keep ~£1m of gross cash headroom and fund growth from EBITDA rather than equity — admirable, and it avoids dilution — but it leaves almost no cushion. If SAWsense conversion slips again, or iTrack disappoints, the self-funding model gets uncomfortable and the equity-raise question reappears. For a ~£7.3m company, that’s the scenario that would hurt most. A small observation is that the company has many years of losses to offset against future profits(so the tax bill would be small). But that’s not something which will drive the share price in the next 5yrs.

Management & governance

The board has genuine AIM pedigree. Nigel Rogers (Executive Chairman) is the architect of the 2020 Bridgestone deal that created the royalty; he’s a chartered accountant (ex-PwC) with 20-plus years running AIM engineers (former Group CEO of Stadium Group and 600 Group, currently also Chairman of Solid State plc). Ryan Maughan (Managing Director) joined in 2021 from an automotive-electrification background to commercialise SAWsense and was promoted to MD in 2025 — he’s the person the growth case is effectively betting on. Melvyn Segal is the long-serving CFO.

Two governance flags worth a line: the Chairman role is combined with an executive remit (common in micro-caps, but not best practice), and the company has form for guidance that proves optimistic — the trajectory from ~157p in early 2025 to 48p today is its own commentary(lets hope things have changed and is now a bit more conservative).

Valuation — a wide cone

I think about this as a sum-of-the-parts plus an option:

- iTrack run-off: ~£2.0–2.2m of near-100%-margin royalty for ~4 more years. Tax-affected and discounted, that’s roughly £5–6m of fairly-certain value on its own — i.e. most of the current ~£6.6m EV.

- Net cash / facility: roughly neutral and tightening — call it negligible net value as the facility is drawn.

- SAWsense + Translogik: the swing factor. Loss-making today, but high-gross-margin with credible blue-chip programmes. This is pure optionality — close to zero in a bear case, and potentially worth multiples of today’s market cap if SAWsense reaches even £5–8m of commercial revenue at these margins.

That framing gives a genuinely wide cone:

- Bear (~40p): iTrack runs off, SAWsense never reaches scale; you’re left near NTA/NAV (32–47p) plus a fading royalty.

- Base (~90p): iTrack normalises around £2m, SAWsense converts a couple of the advanced opportunities into contracted production and the ex-iTrack loss narrows materially by FY28. ≈88% upside from 48p — my headline fair value.

- Bull (180p+): SAWsense inflects on robotics/aerospace volume before 2030, group EBIT scales, and the market re-rates the IP — the territory a genuine commercial inflection would justify.

The asymmetry is real, but it is option-like, not safe: the downside is permanent capital impairment if the self-funding model breaks; the upside needs contracts that haven’t yet been signed.

Risks

- The 2030 cliff. The profit engine has a defined end date; the replacement isn’t proven.

- Conversion risk. SAWsense feasibility-to-NRE-to-production has slipped repeatedly; “shortly” has a poor track record here.

- Revenue quality. Part of SAWsense revenue is grant income, not commercial sales — the underlying paid run-rate is lower than the headline, so “growth” needs reading carefully.

- Cash. Thin net cash, negative FCF, a facility being drawn, stretched receivables. A further slip raises dilution risk.

- Customer concentration / cyclicality. iTrack is FX- and mining-cycle exposed; Translogik leans on tyre majors who just pulled back.

- Liquidity. ~£7.3m micro-cap, 90th-percentile volatility — position-size accordingly.

- Credibility. Repeated downgrades have trained the market to disbelieve guidance, including the company’s own.

What I’m watching (the catalysts)

- Signed contracts, not pipeline. The Chairman flagged imminent wins at the IMC — an RNS naming a contracted SAWsense production order (especially in robotics or aerospace) is the single biggest re-rating trigger.

- The ex-iTrack EBIT line. At the September 2026 finals, the number that matters is segmental profitability excluding iTrack. Any narrowing of that ~£2m loss is the proof the model is turning.

- Commercial vs grant revenue. Evidence that the paid SAW run-rate — not grant income — is what’s growing.

- Cash & the facility. Whether the July collections reverse the year-end working-capital dip as promised, and whether the £900k facility is enough.

- iTrack run-rate. Confirmation that ~£2m is the stable base, not a step on the way down.

Conclusion — speculative, but interesting again

When I sold at ~120p, the story was being priced for flawless execution it then failed to deliver. At 48p, the opposite has happened: the market is pricing little beyond an iTrack royalty in run-off. The truth is in between. This is a genuinely high-quality piece of sensor IP attached to a finite cash engine, run by a capable board, but it is pre-inflection, cash-thin and on a 2030 clock — a special situation, not a sleep-at-night compounder.

The deliberate rebasing of guidance to “highly likely” is, to me, a mild positive — it’s the sort of move a board makes when it wants the next update to beat, and when it can see contracts close enough to mention. If those wins land, the ex-iTrack line starts to turn and the asymmetry pays. If they keep slipping, the royalty melts and the equity gets squeezed.

That’s why I’m treating it as a starter-sized, speculative position with adds reserved for contracted-revenue confirmation rather than a conviction buy today. The thing that flips it from “watch” to “back the truck up” is simple and binary: a signed production contract.

This is my personal analysis for educational purposes and is not investment advice or a recommendation to buy or sell. I may hold a position in the securities mentioned. Micro-cap shares are illiquid and can fall sharply; do your own research and consider professional advice. Forecast figures are drawn from company RNS and broker research; the fair value, rating and any price targets in this note are my own.