The Quick Take

- Company: Advanced Medical Solutions Group (AIM: AMS) — UK-headquartered specialist in tissue-healing technologies, with a global portfolio of surgical adhesives, sutures, haemostats, internal fixation devices, sealants and wound dressings sold under LiquiBand, RESORBA, Peters Surgical, ActivHeal and a dozen other brands

- Thesis: A 35-year-old precision medical device business that has just executed a transformational acquisition (Peters Surgical, July 2024), delivered record financials, recovered its Woundcare segment, and has had five separate PE approaches in 18 months — all of which walked away at indicative prices the board considered too low. The public market is currently pricing AMS at a substantial discount to where serious PE buyers have repeatedly tabled

- Catalyst: The pattern of PE interest is the catalyst. Bridgepoint, Inflexion, Montagu and TA Associates have all looked. None proceeded. With the share price now ~30% below the indicative bid levels they walked away from, the asymmetry has restored itself — and a sixth approach is statistically almost guaranteed

- Valuation: ~194p vs my fair value of 290p (≈49% upside) — anchored to the 270–280p range that recurrent PE buyers find rationalisable on standard LBO mathematics

- Key risk: Cyclically, AMS is exposed to elective surgery volumes and hospital procurement budgets. Structurally, the Peters Surgical integration is still mid-execution and the £10m of operational synergies don’t crystallise until 2027

- Position: Built progressively over the past 18 months; meaningful position in the portfolio

- Time horizon: 12–24 months for the next PE approach to crystallise the value, or 3+ years for the operational story to compound the share price to the same level

I have held AMS for some time and the recent withdrawal of TA Associates’ approach (announced 12 May 2026) is the trigger for putting a more formal initiation note on the blog. The shares have drifted back from around 240p during the bid period to ~194p today, restoring the public-market discount that has, by now, drawn five separate PE firms to AMS’s door in the past eighteen months. That is not normal. And the reason for it — the unusual combination of a defensible niche, recurring revenue, conservatively-managed balance sheet and unused debt capacity — is the reason this stock deserves a proper write-up rather than a quick commentary.

What AMS actually does

Advanced Medical Solutions is, in plain terms, a specialist medical device manufacturer focused on the moment when human tissue is cut, torn, or otherwise damaged — and on the technologies that close, seal, heal or otherwise repair that tissue. The business operates across two segments — Surgical (around 80% of FY25 group revenue) and Advanced Woundcare (around 20%) — but the underlying product set is a remarkably broad portfolio of niche-leading positions in spaces where the customers are surgeons, theatre teams and wound-care specialists across more than 70 countries.

Founded in 1991 in Winsford, Cheshire, the group has 1,600 employees and manufacturing operations spread across the UK, Germany, France, Thailand and India. The bedrock product is LiquiBand, the family of cyanoacrylate tissue adhesives used to close surgical wounds and lacerations in place of (or in combination with) sutures. The benefits are well-documented in clinical literature: faster closure, better cosmetic outcomes, lower infection rates, no follow-up suture removal. LiquiBand competes globally with Ethicon’s Dermabond, and the Surgical division has built a strong position particularly in the US.

Around LiquiBand sits a constellation of acquired and developed adjacent technologies: RESORBA sutures and biosurgical implants (acquired 2017), LiquiBandFix8 mesh fixation devices, Sealantis internal sealants, Syntacoll collagen-based absorbable implants (acquired 2023), and most importantly Peters Surgical, the transformational July 2024 acquisition which more than doubled the Surgical revenue base. The Woundcare segment supplies advanced dressings — silver alginates, alginates, foams — under the ActivHeal brand and through white-label private-label channels.

The aggregate proposition is a portfolio of niche-leading medical devices with deep clinical evidence, established regulatory positions across major geographies, sticky hospital procurement relationships, and a manufacturing footprint that produces a high mix of own-IP product alongside contract manufactured volume. None of it is exciting in the way an AI semiconductor business is exciting. All of it is, in PE jargon, “highly cash-generative defensive growth” — and that is exactly the kind of asset that financial buyers spend their careers searching for.

The two segments

AMS reports across two operating segments, and the recent dynamics within each are worth understanding.

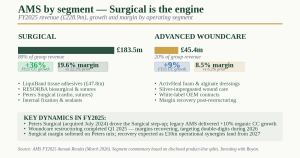

Surgical (~80% of FY25 group revenue, £183.5m, +36% constant currency). The growth engine of the business and the dominant earnings driver. Within Surgical, the headline product family is Advanced Closure (LiquiBand and adjacent tissue adhesives) at £47.8m in FY25 (+12% CC), with strong US growth of 13% CC driven by the longer-wound LiquiBand XL launch. Biosurgical and Sutures is the larger and faster-growing sub-segment, materially expanded by the Peters Surgical acquisition; product categories include cardiac sternotomy closure (a Peters specialty), specialty sutures, mechanical haemostasis devices, internal sealants and biosurgical implants. The legacy AMS Surgical business (excluding Peters) delivered 10% constant currency organic growth in FY25 — a healthy print that validates the core is performing on its own merits, not just being flattered by the acquisition. Adjusted operating margin for Surgical was 19.6% in FY25, down from 22.2% in 2024 due to acquired-business mix (Peters runs lower gross margins than legacy AMS) and integration costs; this is expected to recover as synergies flow through.

Advanced Woundcare (~20% of FY25 group revenue, £45.4m, +9%). The smaller and more cyclical segment, supplying foam dressings, alginates, silver-impregnated products and bulk wound-care materials under both the ActivHeal brand and through white-label OEM contracts with global wound-care companies. The segment had been a profitability drag through 2023–2024 due to inflationary cost pressure and adverse mix, and underwent a focused restructuring programme completed in Q1 2025. The recovery has been visible: Infection and Exudate Management revenue grew 14% to £42.1m, and the adjusted operating margin recovered to 8.5% (from 6.2% in 2024). Management has guided that Woundcare margins should move into double-digits during 2026.

The strategic intent across both segments is clear: focus capital, R&D and commercial attention on the higher-margin Surgical franchise where AMS has differentiated IP and clinical evidence; manage Woundcare as a stable, cash-generative bolt-on platform that supplies the cash flow to fund Surgical’s growth ambitions. After several years of mixed signals, both segments are now executing on this model.

The Peters Surgical deal and the integration narrative

The Peters Surgical acquisition, completed 1 July 2024 for an initial €132.5m (~£113m) plus an earnout of up to €8.9m, is the most consequential strategic move AMS has made in its history. Peters Surgical was a French-headquartered global provider of specialty surgical sutures, mechanical haemostasis devices and cyanoacrylate-based products with FY23 revenue of €84m. The strategic logic is compelling on three levels.

First, it nearly doubled the Surgical segment in revenue terms, taking AMS from a sub-£200m group to a £228m group at the FY25 reporting line. That scale matters disproportionately in a fragmented surgical specialty market where global hospital procurement contracts increasingly favour multi-product suppliers.

Second, Peters brought genuinely complementary product capability — specifically in cardiac sternotomy closure and specialty sutures — that AMS lacked. The cross-selling opportunity through Peters’ established cardio-vascular sales channels is the highest-visibility commercial synergy and is already contributing in FY25.

Third, the operational synergy programme is meaningful: management has guided to £10m of annual operational synergies from 2027, on top of the commercial synergies already being banked. £10m of synergies on a £50m EBITDA base is a 20% earnings uplift just from integration execution — not from any organic growth or market expansion. If delivered, that’s where the genuine medium-term EPS leverage comes from.

The integration progress through FY25 has been on track. Both Peters Surgical and the smaller Syntacoll acquisition (collagen-based absorbable implants) are integrating cleanly. Some near-term headwinds — destocking in the Peters B2B channel, legacy supply issues and US tariff-related order phasing — have constrained FY25 reported revenue slightly below what an undisturbed business would have shown, but the underlying delivery is sound.

The PE thesis: why financial buyers keep coming back

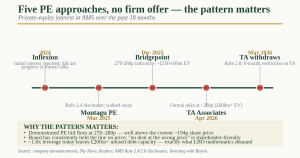

This is the section that distinguishes AMS from a routine medtech initiation. Five PE firms in eighteen months — Inflexion (2024), Montagu (March 2025), Bridgepoint (December 2025), TA Associates (April 2026), and another rumoured at the periphery of the Bridgepoint period — have looked seriously at acquiring AMS. None has proceeded. The question is why this pattern, and what it tells you about fair value.

The answer is mathematical rather than mysterious.

AMS at 194p has a market capitalisation of approximately £419m on 216m shares outstanding. Net debt at FY25 year-end was £50.5m, so enterprise value is approximately £470m. FY25 adjusted EBITDA was £49.9m. EV/EBITDA is therefore approximately 9.4x trailing, or about 8.5x on FY26E EBITDA of £55m. For a specialty medical device business with leading positions in tissue adhesives, sutures, biosurgical implants and wound care, with 80%+ recurring revenue, with margins recovering and integration synergies still to be banked, that is genuinely cheap.

But the LBO maths is where the PE attraction really shows. AMS has been deleveraging rapidly since the Peters Surgical deal — net debt fell from £55.8m at FY24 year-end to £50.5m at FY25, despite paying a growing dividend. The trajectory points to roughly £30–40m net debt by end-2026. On £55m+ EBITDA, that’s around 0.5–0.7x leverage — exceptionally conservative for a defensive growth business. PE houses routinely operate businesses at 4–5x leverage. The implied unused debt capacity is therefore £200m+. That is not theoretical: it is exactly the lever an LBO sponsor would deploy.

The standard PE playbook looks something like this: take AMS private at, say, 290p (around £626m equity value), inject £150m of leveraged debt to take total net debt to £180m (around 3.3x), redeem most of the equity within 12–18 months via a dividend recap, hold for 4–5 years while executing the Peters Surgical synergies and modest geographic expansion, exit via secondary sale or IPO at 7–8x money invested. That’s the model. It works on a 9x EV/EBITDA entry multiple. It works far better on a 12x exit multiple if a strategic acquirer pays up.

Multiple PE houses arriving at the same conclusion is therefore not coincidence. It is the expected outcome of running the same spreadsheet model on a public asset that screens unusually well.

The reason none has proceeded is also mathematical. Bridgepoint’s indicative was reportedly 270–280p; TA Associates was preparing around 280p. Deutsche Bank’s published research called 280p “not a knock-out figure” and the bank’s own price target sits at 275p. The board has clearly held the line on price, declining to recommend at indicative levels where the PE sponsor’s IRR works but the public-shareholder return is uncompelling. That posture is correct and shareholder-friendly. It is also why the recurring approaches have, so far, each ended at the “intent to walk away” stage rather than at a firm offer.

The implications are threefold. First, there is now an effective price floor of 270–280p for any future PE bid — a sixth approach below that level would be summarily dismissed. Second, the operational delivery (Peters synergies, US regulatory wins, Woundcare margin recovery) continues independently of the M&A activity, so the intrinsic value compounds while shareholders wait. Third, the Rule 2.8 restriction on TA Associates only binds that one firm for six months — other PE houses are unconstrained, and several have already demonstrated they think the asset is worth bidding for.

Financial shape: record year, healthy balance sheet, dividend growing

The FY25 financials are the cleanest set the group has produced in some years.

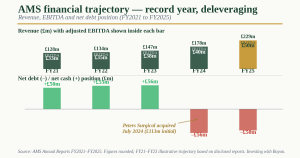

Revenue. FY25 revenue of £228.9m grew 29% on a reported basis from £177.5m in FY24, supported by the first full year of Peters Surgical contribution alongside good organic growth across both segments.

Profitability. Adjusted EBITDA grew 24% to £49.9m, with the margin slightly lower at 21.8% (vs 25.3% in H1 2024 standalone) reflecting acquired-business mix. Adjusted operating profit was around £30m. Reported pre-tax profit jumped 81% to £17.8m, partly reflecting the prior year being depressed by Peters acquisition-related exceptional items.

Cash generation. Net operating cash flow was £32.6m, up 67% — a meaningful step-up reflecting both the acquisition-enlarged EBITDA base and normalised working capital after the integration period.

Balance sheet. Net debt of £50.5m at FY25 year-end versus £55.8m at FY24, representing leverage of approximately 1.0x EBITDA on the trailing basis. The deleveraging trajectory is clear and points to a sub-1x leverage position by end-FY26.

Capital returns. Total dividend of 2.86p for FY25, up 10% on prior year, comfortably covered by operational cash generation. AMS does not currently run a buyback programme — capital allocation priority is deleveraging and bolt-on M&A — but in a non-bid scenario, capital returns could plausibly accelerate from here as leverage normalises.

Forward outlook. Management has guided 2026 revenue and EBITDA in line with market expectations. The published consensus expects revenue growth of mid-single-digits and EBITDA expansion to ~£55m as Peters synergies start to crystallise. US regulatory programmes for biosurgical and suture products are progressing and underpin medium-term Surgical growth. Woundcare margins should move into double digits during 2026.

Valuation

At ~194p, AMS’s market capitalisation is approximately £419m on 216m shares outstanding. The current valuation framework is unusual because of the dual benchmark — public market multiples on one hand and the demonstrated PE bid range on the other.

On public-market metrics: trailing P/E is approximately 12x adjusted earnings; forward P/E is approximately 10x consensus FY26 EPS; EV/EBITDA is 9.4x trailing, 8.5x forward. Trailing dividend yield is 1.5%. For a defensive growth medtech business with leading positions in attractive niches, double-digit organic growth in Surgical, integration synergies still to land, and a deleveraging balance sheet, those multiples are conservative.

On the PE benchmark: Bridgepoint and TA Associates both indicatively valued AMS in the 270–280p range, with the AMS board considering even those levels insufficient. Deutsche Bank’s published target is 275p. The Stockopedia analyst consensus target is 276p. These reference points cluster tightly in the 270–290p range.

My fair-value framework:

- Bull case (~320–360p, 65–85% upside). A sixth PE approach materialises within 12 months at a level that closes the gap to the board’s expected price — likely 300–320p. The Peters Surgical synergies deliver on schedule, Woundcare margins move into double digits, US regulatory approvals land, and FY27 EBITDA reaches £62m+. Multiple sustained at 11–12x EV/EBITDA on growing earnings. A successful sale to a strategic buyer (medical device peer with global commercial reach) prices higher than a financial buyer due to revenue synergies, potentially in the 350p+ range.

- Base case (~280–300p, 44–55% upside). No firm bid materialises in the next 12 months, but the operational story compounds. FY26 EBITDA at £55m delivered, deleveraging continues, Peters synergies bank on schedule. Share price gradually re-rates to the level that recurrent PE buyers have demonstrated they are willing to pay — the 270–280p floor becomes the new trading range, with the operational compounding then taking the equity to 290–300p over 18 months.

- Bear case (~150–180p, 7–23% downside). Peters integration hits an unexpected friction; surgical procedure volumes soften meaningfully (a possible scenario in a recession); a major US tariff event disrupts the supply chain; Woundcare margin recovery stalls. Net debt remains higher for longer, dividend growth slows, public market multiple compresses to 7–8x EV/EBITDA. Share price drifts toward the 52-week low.

Probability-weighting (40% bull / 45% base / 15% bear) gives a central fair value of approximately 290p on a 12–18 month view — roughly 49% upside from current levels. The probability tilt toward the bull case reflects the unusual asymmetry created by the recurring PE interest: even in a no-deal scenario, the demonstrated PE bid floor at 270–280p effectively underpins downside protection while the bull case retains optionality on a higher strategic outcome.

Key risks

I would be misleading anyone if I left these out:

- No PE bid is guaranteed. Five approaches in eighteen months has not produced a single firm offer. The pattern may simply reflect that AMS is almost an LBO candidate but not quite at the price PE wants — and the board’s posture means the gap never closes. In that scenario, the equity is dependent on operational delivery alone, and the catalyst-driven upside disappears.

- Integration execution risk. Peters Surgical and Syntacoll are both still mid-integration. The £10m operational synergy target for 2027 requires execution against milestones that have plenty of room to slip. Any meaningful integration cost overrun or delivery delay would directly compress the EBITDA trajectory.

- Surgical procedure volume sensitivity. AMS revenue is closely tied to elective surgery volumes and global hospital procurement budgets. A meaningful recession that reduced elective procedure volumes (which has happened multiple times historically) would translate quickly into revenue softness.

- Competition in core franchises. LiquiBand competes globally with Ethicon’s Dermabond and other tissue adhesive brands. RESORBA sutures compete with Ethicon’s market-leading suture franchise. AMS holds defensible positions but competes against very large strategic players with deep commercial reach.

- Currency exposure. AMS reports in GBP but a meaningful proportion of revenue is non-GBP (USD, EUR particularly post-Peters). Sterling strength is a translational headwind that has affected reported numbers through 2024–2025.

- AIM small-cap profile. AMS is the largest position on this initiation list in absolute market cap terms (£419m), but it remains AIM-listed with the associated liquidity and institutional-mandate constraints. Index inclusion in the FTSE All-Share would require a Main Market move which is not on the company’s stated strategic agenda.

- Tariff exposure. Some Peters Surgical products face US tariff exposure that has materially affected order phasing in 2025. Management commentary suggests this is being actively managed, but the issue is structural rather than transient.

- Operating margin trajectory. Group adjusted EBITDA margin dropped from above 23% pre-Peters to 21.8% in FY25. The recovery to 23-24% relies on Peters integration synergies and Woundcare margin progression. Either of those slipping materially would constrain the equity story.

What I’m watching from here

Three concrete operational tests will define the next 12 months:

- A sixth PE approach. The pattern says one is likely. The price level it arrives at — and whether the board engages or dismisses — will tell you everything about where they see fair value. Watch the share register filings for unusual institutional positioning and any Sky News or Reuters speculation; these have preceded every recent approach.

- H1 2026 results (likely September 2026). The first reporting period showing meaningful Peters synergy contribution and a clean Woundcare margin print. The H1 EBITDA margin trajectory is the critical operational data point.

- US regulatory progress. Biosurgical and suture programmes are working through the FDA pathway. Approvals would unlock the US market for additional Peters Surgical products — a meaningful incremental revenue opportunity that public-market analysts have not yet fully modelled.

If those three boxes tick — a sixth PE approach, clean H1 numbers, US regulatory wins — the share price should approach the upper end of my bull case. If the operational story disappoints and no further PE interest materialises, the share price reverts to operational fundamentals alone, and the 280–300p target becomes a 2–3 year journey rather than a 12-month catalyst.

In summary, Advanced Medical Solutions is a high-quality medical device business that the public market is currently pricing 30%+ below where five separate sophisticated PE buyers have demonstrably been prepared to bid. The board has held the line on price, correctly in my view, and the deleveraging trajectory means each passing quarter increases the unused debt capacity that makes AMS attractive to financial buyers in the first place. The Peters Surgical integration is on track, the Woundcare segment has recovered, capital returns are growing, and the underlying clinical proposition has multi-decade durability. The structural set-up — a private-market floor demonstrated repeatedly above a public-market price — is unusual and asymmetric. For me, that fits comfortably as a meaningful position with capital-return potential through either an eventual bid or simple operational compounding.

Disclosure: I hold a position in Advanced Medical Solutions at the time of writing. This is not investment advice — always do your own research. Read the full disclaimer at investingwithboyan.com.

If you found this useful, more analysis is available at investingwithboyan.com — or subscribe via the form in the sidebar to get new pieces straight to your inbox.