MTI Wireless Edge (AIM: MWE) – Initiation of Coverage

MTI Wireless Edge (AIM: MWE) — Initiation of Coverage

The Quick Take

- Company: MTI Wireless Edge (AIM: MWE) — Israeli antenna and defence-comms group

- Thesis: Net-cash AIM compounder mispriced as a sleepy small-cap; the PSK Wind defence pivot is materially under-appreciated

- Valuation: ~68p vs my fair value of 100p (≈47% upside)

- Key risk: Defence revenue is lumpy; PSK execution still unproven at scale

- Position: Starter — added in March, will add on weakness

- Time horizon: 2–3 years

I’ve recently added MTI Wireless to the portfolio, alongside the names covered in my Q1 26 portfolio update. The shares are up roughly 20% month-to-date on a string of contract wins, so I’m late to write this one up — but the investment case is strong enough that I’d still be a buyer at current levels.

What MTI actually does

MTI Wireless Edge is an Israeli technology group that builds the unglamorous but essential plumbing of modern wireless communication: antennas, wireless links and remote-control infrastructure, now augmented by a growing defence-communications arm via PSK Wind. It sits on AIM with a net-cash balance sheet, a portfolio of niche, mission-critical products and a valuation that still assumes this is a sleepy small-cap rather than a steadily compounding operator.

On the surface, the group looks eclectic: antennas for everything from 5G backhaul to naval platforms, a water-control business built on Motorola’s IRRInet technology, a specialist wireless-component distributor, and a majority stake in PSK Wind, a turnkey provider of integrated communication stations for defence customers. Underneath, though, all of these activities share a common thread — deep expertise in sending and receiving information wirelessly and reliably in harsh environments.

The four divisions

Antennas. The technological core. Designs and manufactures antennas for 5G backhaul, broadband, public safety networks, RFID and utility infrastructure — plus tactical and specialised antennas for airborne, naval, ground and submarine platforms. This is the long-term value engine of the group.

Water Control & Management (Mottech). Remote monitoring and control systems for irrigation, municipal water distribution, wastewater and storm-water reuse, built on Motorola’s IRRInet platform. A steady, contract-driven business with clear ESG tailwinds.

Distribution & Professional Consulting (MTI Summit). Represents overseas suppliers of wireless and microwave components, and provides engineering, integration and support services for aerostat, radar, signals-intelligence and communication systems.

PSK Wind. Majority-owned subsidiary delivering fully integrated communication stations, shelters and infrastructure projects for defence and government customers. Increasingly focused on high-end command-and-control and monitoring installations.

Strip away the labels and what MTI really sells is specialised wireless connectivity and remote-control infrastructure — antennas, links, control systems, shelters, and long-term service contracts that keep critical networks running.

PSK Wind: the defence-grade glue

This is the part of the story I think the market is missing.

PSK Wind sits at the intersection of MTI’s defence ambitions and its systems-integration skills. Where MTI Summit historically sold components into defence projects, PSK lets the group sell the entire site — infrastructure, power, communications hardware, and the monitoring and control systems that tie it all together. That’s a structurally higher-value, higher-margin proposition with embedded multi-year service revenue.

After a difficult 2024, PSK entered 2025 with what management described as a “very healthy order backlog” and a long pipeline driven by rising government defence investment. Since then, multiple contract wins for integrated shelters and defence services worth around US$1m+ each have been announced.

Crucially, MTI Summit has increased its stake in PSK from 51% to 60% through additional equity investment, with options to acquire the remaining 40% from 2027. That’s a strong management signal — they’re voting with the chequebook that PSK is past its teething problems and ready to scale.

Financial shape: asset-light and cash-rich

The financial profile is more solid than the share price suggests:

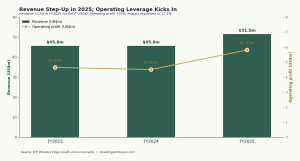

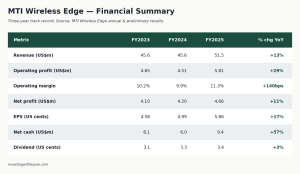

Growth and margins. Recent results show revenue stepping into the low-US$50m range, with operating profit growing materially faster than sales as higher-margin antennas and defence-related work scale. Operating margins in the high single digits to low double digits are respectable for a business dealing primarily in engineering and integration rather than heavy manufacturing.

Balance sheet. MTI runs with net cash, which increased further in 2025 despite continued investment and tuck-in deals. Genuine strategic flexibility in a market where many peers are still cleaning up over-levered balance sheets.

Capital returns. A track record of rising dividends and share buybacks while still funding organic growth and bolt-ons. The payout remains well covered by earnings, leaving ample room to keep investing in new antenna platforms, water deployments and PSK projects.

Valuation

I get to a fair value of around 100p using a sum-of-the-parts approach: a low-double-digit multiple on the antenna and defence earnings (justified by the recurring nature and growth profile), the water and distribution divisions valued more conservatively, and net cash added at face value.

At today’s 68p, the market is essentially valuing MTI as a static small-cap component supplier and ignoring both the operating leverage in the antenna business and the optionality embedded in PSK. The recent contract wins suggest that gap is starting to close — but there’s still meaningful runway.

Key risks

I’d be misleading anyone if I left these out:

- Defence revenue is lumpy. Contract timing can swing quarterly numbers materially. PSK is still small enough that one delayed project moves the dial.

- Geopolitical concentration. A meaningful share of the order book is Israeli or Israel-adjacent. The current security environment is a tailwind for defence demand, but introduces obvious risk in the underlying operations.

- PSK execution. The strategic logic is clear, but PSK had a difficult 2024 and the stake increase to 60% only just happened. I’ll be watching the next set of results closely for confirmation of margin progression — not just top-line.

- FX exposure. Reporting in US dollars with a meaningful Israeli shekel cost base. A weakening dollar against the shekel pressures margins.

What I’m watching from here

The next set of half-year results is the key test for the PSK thesis. Three things I want to see:

- PSK’s contribution to group EBIT growing faster than its revenue (i.e. margin progression).

- Continued antenna order momentum, particularly in defence-adjacent applications.

- Net cash holding or rising despite the increased PSK investment.

If those three boxes tick, I’ll be adding meaningfully. If PSK margins disappoint or the antenna business shows signs of slowing, the 100p target needs to come down.

Disclosure: I hold a position in MTI Wireless Edge at the time of writing. This is not investment advice — always do your own research. Read the full disclaimer here.

If you found this useful, you can get new analysis straight to your inbox —please subscribe via the form in the sidebar.