Distribution Finance Capital (AIM: DFCH) — Initiation of Coverage

The Quick Take

- Company: Distribution Finance Capital Holdings (AIM: DFCH), trading as DF Capital — a specialist UK bank providing inventory (“floorplan”) finance to manufacturers, dealers and distributors across leisure, marine, powersports, industrial, agricultural and automotive sectors, funded by a digital retail savings franchise

- Thesis: A young, profitable, fast-growing niche bank with a genuinely clear and credible business plan — record 2025 results, a loan book compounding at ~27%, pristine credit quality, and a path to a £1.5bn loan book and ~20% returns by 2030, funded organically without dilution. It trades at roughly 7x earnings and around 0.76x tangible book — a discount to its tangible net asset value of 75.9p per share

- Catalyst: The January trading update (followed by full results in March) was exceptional — loan book +27% to £846m, adjusted PBT +26% to £18.1m, cost of risk of just 0.59%. The new DFRNT asset-finance product opens a market several times larger than the core

- Valuation: ~54p vs my fair value of 80p (≈48% upside). The shares trade at ~0.76x tangible book (TNAV of 75.9p per share) and ~7x earnings — cheap for a bank targeting ~20% returns, with the discount reflecting the one risk that genuinely matters for this business: cyclicality

- Key risk: This is an inventory-finance lender, and inventory finance is cyclical. In a recession, dealer demand falls, used-asset values drop, and arrears rise — all at once. The credit quality is pristine today, but it has not yet been tested through a genuine downturn under the current scale

- Position: Bought around 40p, sold the lot at 55p, then bought back at 58p after the January results convinced me the plan was on track.

- Time horizon: 3-5 years to deliver the 2030 plan; the re-rating should come sooner if credit quality holds through 2026-27

A word on why I am writing this up at all, because it is a slight departure for me. I generally avoid financials. Banks are complex, opaque, highly leveraged by their very nature, and it is genuinely hard for an outside investor to know what is sitting inside a loan book until it is too late. The history of bank investing is littered with cheap-looking lenders that turned out to be cheap for a reason. So my default with this sector is to pass.

DF Capital is the exception, for one simple reason: the business plan is unusually clear, and the company has been executing against it with metronomic consistency. This is not a sprawling universal bank with a trading book and exposures I cannot understand. It is a focused, single-product specialist doing one thing — lending money to dealers to hold stock — and doing it well. My own history with the shares reflects that conviction building: I bought around 40p, took profit and sold the entire holding at 55p, and then bought back at 58p after the January results. Selling and then rebuying higher feels like an error on the surface, but the January numbers materially de-risked the plan in my eyes, and I would rather own a strengthening thesis at 58p than sit out of one I understand. The one thing that stops me sizing this larger is the cyclicality — which I will come to.

What DF Capital actually does

DF Capital is a specialist bank, and its core product is something called inventory finance — also known as floorplan finance, stocking finance, or wholesale finance. It is one of the oldest and most practical forms of commercial lending, and once you understand it, the business becomes very easy to follow.

Picture a dealer — say, a caravan and motorhome dealership. To make sales, the dealer needs physical stock on the forecourt: a range of caravans for customers to see, touch and buy. But that stock is expensive, and the dealer’s cash is finite. Buying a forecourt full of caravans outright would tie up enormous amounts of working capital. So instead, the dealer uses inventory finance: DF Capital pays the manufacturer for the stock, and the dealer holds it on the forecourt under a financing arrangement, paying interest on the financed amount until the unit is sold. When a customer buys a caravan, the dealer repays DF Capital for that unit and the cycle continues.

Everyone in the chain benefits. The manufacturer gets paid promptly and can keep producing. The dealer can hold far more stock than its own cash would allow, driving more sales. And DF Capital earns interest on the financed inventory, secured against physical, identifiable, resaleable assets. It is working-capital plumbing for the distribution economy, and it is genuinely useful.

DF Capital operates across a deliberately diversified set of sectors — leisure (caravans, motorhomes, lodges, holiday homes), marine (boats), powersports (motorcycles, ATVs), industrial and agricultural equipment, and specialist automotive. This diversification is a deliberate risk-management choice: no single end-market dominates the book, so a downturn in one sector does not sink the whole portfolio. The company works with around 97 manufacturers and nearly 1,500 dealers, serving over 13,000 active customer relationships through a highly digitised online platform run from its Manchester base.

Founded in 2016 and granted a full UK banking licence in September 2020, DF Capital has grown into a genuine bank with around 150 staff. Its subsidiary, DF Capital Bank Limited, holds the licence and the deposits.

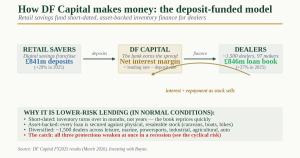

How the model works: the deposit-funded flywheel

The thing that turns DF Capital from a lender into a bank — and the thing that makes the economics work — is how it funds its lending.

DF Capital funds its loan book primarily through retail savings deposits. It runs an award-winning digital savings franchise, offering competitive fixed-term and notice savings accounts to UK consumers and small businesses. Those deposits — £841m at the end of 2025, up 29% — provide the funding for the inventory-finance loan book of £846m. The bank earns a higher rate of interest on the lending than it pays out on the deposits, and the difference — the net interest margin (NIM) — is the core of its profitability.

This is the classic banking model, but applied to a single, well-understood, asset-backed lending niche. The flywheel works like this: a strong savings franchise brings in low-cost, stable deposits; those deposits fund a growing, well-secured loan book; the loan book generates net interest income; that income, after costs and loan losses, becomes profit; profit builds capital (tangible net assets); and a stronger capital base supports a still-larger loan book. Round it goes. The genius — and the risk — of banking is that this flywheel is leveraged: a relatively small base of equity capital supports a much larger book of loans and deposits.

What makes DF Capital’s version attractive is that the lending is short-dated (inventory turns over in months, not years), secured against physical assets, and spread across thousands of dealers and multiple sectors. Short-dated, secured, diversified lending is about as low-risk as bank lending gets — in normal conditions.

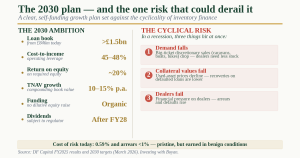

The growth story and the 2030 plan

The reason DF Capital screens as more than just a cheap small-cap bank is the clarity and credibility of its growth plan.

At the January trading update and confirmed in the March results, management laid out a set of medium-term targets extending to 2030: a loan book of more than £1.5bn (from £846m today); a cost-to-income ratio of 45-48% (reflecting the operating leverage of a scalable digital platform); a return on required equity of around 20%; and tangible net asset growth of 10-15% per annum. Critically, management expects to fund all of this organically — from retained earnings and existing capital tools — without any dilutive equity raise. They have even signalled the potential for buybacks, portfolio acquisitions, and the initiation of dividends after the 2028 financial year, subject to regulatory approval.

There are two growth engines. The first is continued share gains in the core inventory-finance market, where DF Capital keeps adding manufacturers and dealers and is taking share in resilient but underserved niches. The FY2026 closing loan book is already guided to exceed £900m.

The second, and more interesting, is the new DFRNT asset-finance product, launched in 2025 after the bank secured the necessary consumer-lending approvals. Where inventory finance funds the dealer’s stock, asset finance funds the end customer’s purchase of that stock — a fundamentally larger market. DF Capital can now offer financing at both ends of the same transaction, to the same network of manufacturers and dealers it already serves. Management notes that this existing base represents over £10bn of annual sales — so even modest penetration of that flow with asset finance represents a material expansion of the addressable market. DFRNT lent its first £15.6m in year one across around 120 dealers and introducers. It is small today but is the single most important medium-term growth optionality in the business.

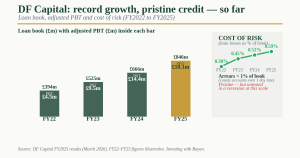

Financial shape: record year, pristine credit — so far

The 2025 results were, by any measure, excellent.

Loan book. Up 27% to £846m (FY24: £666m), driven by a diversified mix of inventory, structured and asset finance across the target sectors. New loans advanced in the year exceeded £1.8bn (up 27%), reflecting the high-turnover nature of inventory lending.

Deposits. Up 29% to £841m, comfortably funding the loan book and reflecting the strength of the digital savings franchise.

Revenue and profit. Gross revenue grew 19% to £90.9m (FY24: £76.7m). Adjusted profit before tax rose 26% to £18.1m (FY24: £14.4m), with statutory PBT of at least £19m. The profit grew faster than revenue thanks to a higher net interest margin, an improved cost-to-income ratio (the operating leverage of the digital platform showing through), and disciplined cost control.

Credit quality. This is the critical line for any lender, and DF Capital’s 2025 numbers were pristine. The cost of risk — loan losses as a percentage of the book — was just 0.59%. Arrears and non-performing loans remained below 1% of the book. It is worth stressing how conservative that arrears figure is: DF Capital defines arrears as any account even a single day past its due date, so the sub-1% number captures every account that is so much as one day late, not just loans in serious default. On that demanding definition, sub-1% arrears is genuinely impressive. For an asset-backed, short-dated, diversified lending book, that is exactly what you would hope to see.

Capital and returns. Tangible net asset value stood at 75.9p per share, with the bank compounding tangible book by 19% in 2025 — ahead of its 10-15% per annum medium-term ambition. The bank is generating capital organically, which is what underpins the “no dilution required” promise in the 2030 plan. Return on required equity is improving toward the 20% medium-term target, though the blended return on total tangible equity remains lower for now because the bank holds surplus capital above its regulatory requirement that has yet to be fully deployed into the loan book.

At ~54p, the shares trade at roughly 7x trailing earnings and around 0.71x tangible book value — that is, below the 75.9p of tangible net assets per share that sit behind each share. For a bank growing its loan book at 27%, compounding tangible book value at double digits, and targeting a 20% return on required equity, a share price below tangible book is — on the face of it — cheap. The question, as ever with banks, is whether the credit quality that makes those earnings real will hold.

Valuation

Banks are best valued on two measures: a multiple of earnings, and a multiple of tangible book value (cross-checked against the return on equity the bank generates).

On earnings: at ~54p, with trailing earnings of roughly 8p per share, DF Capital trades at approximately 7x. For a business compounding earnings at 20%+, that is a low multiple — a sub-1x PEG, in old-fashioned terms.

On tangible book: at around 0.71x tangible net assets (75.9p per share against a ~54p share price), the market is pricing DF Capital at a discount to its tangible book value — in effect valuing the whole bank below the net assets that sit behind it. There is an important nuance here. The ~20% target is a return on required equity (the regulatory minimum capital), and the bank currently holds surplus capital above that requirement, so its return on total tangible equity is lower for now — in the low-teens rather than 20%. As the loan book scales toward £1.5bn, more of that surplus capital gets deployed at the higher marginal return, and the blended return on tangible equity should climb toward the high-teens. A bank earning a sustained high-teens return on tangible equity should not trade at a discount to book; it should trade at a premium. The gap between the 0.71x the shares trade at today and the 1.0-1.3x a rising return profile would justify is the re-rating opportunity, if the returns prove durable through the cycle.

My fair-value framework:

- Bull case (~95-110p, 64-90% upside). The 2030 plan delivers broadly on schedule: the loan book compounds toward £1.5bn, DFRNT asset finance scales meaningfully, the cost-to-income ratio falls to the target 45-48%, and return on required equity reaches ~20%. Credit quality holds through the period. The market re-rates the shares toward 1.2x tangible book (on a book that is itself compounding) and 10-12x earnings on a much larger earnings base.

- Base case (~75-85p, 29-47% upside). Continued solid execution — the FY26 loan book exceeds £900m, DFRNT grows steadily, returns improve toward the high-teens, credit stays benign — and the market closes the discount to trade at roughly 1.0x tangible book and ~9-10x earnings. No recession, no credit shock, just consistent compounding and the share price converging on a steadily rising tangible book value.

- Bear case (~38-46p, 21-34% downside). A UK recession hits the cyclical core of the business: dealer demand softens, used-asset values fall (reducing the value of the collateral securing the book), dealer failures rise, and the cost of risk climbs from 0.59% toward the 2-3%+ seen at lenders in past downturns. Loan-book growth stalls or reverses, earnings compress, and the market de-rates the shares to roughly 0.5x tangible book. This is the scenario that the cyclicality of inventory finance makes a genuine possibility.

Probability-weighting (35% bull / 45% base / 20% bear) gives a central fair value of approximately 80p on a 12-18 month view — roughly 48% upside from current levels, and only modestly above the current 75.9p tangible book value. That is a deliberately conservative anchor: I am giving real weight to the cyclical downside rather than assuming the execution case plays out unimpeded. I think the execution case is very likely to play out in the absence of a recession — but the whole point about cyclical lenders is that the downside, when it comes, comes quickly and severely, and a fair value has to carry some weight on that tail.

Key risks

The risks here are, unusually, dominated by a single one — and it is the one I want to be most honest about.

- Recession and the credit cycle — the risk that matters most. Inventory finance is cyclically geared in a way that compounds in a downturn. In a recession, three things happen at once, and they reinforce each other. First, consumer demand for big-ticket discretionary items (caravans, boats, motorcycles) falls, so dealers sell fewer units and need less stock financing — the loan book shrinks. Second, used-asset values fall, which erodes the value of the collateral securing the existing book, so recoveries on defaulted loans are lower. Third, dealers themselves come under financial pressure, so defaults and arrears rise. A lender can withstand any one of these; it is the simultaneity that makes a downturn dangerous for floorplan finance. DF Capital’s cost of risk of 0.59% and sub-1% arrears are genuinely excellent — but they have been earned in benign conditions, and the business has not yet been tested through a real recession at its current scale. This is the single reason I size the position modestly and anchor my fair value at a conservative ~1.0x tangible book rather than the premium a 20%-return bank would otherwise justify.

- Leverage is inherent. As a bank, DF Capital is leveraged by design — a relatively thin slice of equity supports a much larger book. That magnifies returns on the way up and losses on the way down. The regulatory capital framework is there precisely to manage this, but leverage always amplifies credit shocks.

- Funding and deposit competition. The model depends on attracting retail deposits at a competitive cost. In a period of intense deposit competition or rapidly changing interest rates, funding costs could rise faster than lending yields, compressing the net interest margin.

- Interest-rate sensitivity. As a spread lender, DF Capital’s profitability is sensitive to the path of interest rates and to how quickly its lending and deposit rates reprice relative to each other.

- Execution risk on DFRNT. The new asset-finance product is a genuinely new lending discipline (consumer rather than wholesale credit), with a different risk profile. Scaling it well is a meaningful medium-term opportunity; scaling it badly would introduce credit losses in an unfamiliar area.

- Small-cap and liquidity. AIM-listed, ~£97m market cap, with variable daily liquidity. Exiting a position in a stressed market could be difficult.

- Regulatory. As a licensed bank, DF Capital operates under PRA and FCA supervision. Changes to capital requirements, conduct rules or the regulatory treatment of its products could affect the economics or the growth plan.

What I’m watching from here

Three things will tell me whether the thesis is on track over the next 12-18 months:

- Cost of risk and arrears. This is the single most important number to monitor. As long as the cost of risk stays below ~1% and arrears remain benign, the loan-book growth is high quality and the earnings are real. Any sustained climb in the cost of risk — especially ahead of an actual recession — would be the early warning that the cycle is turning.

- DFRNT asset-finance scaling. The first £15.6m was a start. I want to see the asset-finance book growing steadily through 2026, with credit performance in line with the core book. This is the growth optionality that could take the medium-term plan from “solid” to “excellent.”

- Loan-book and margin trajectory. The FY26 closing loan book is guided above £900m. Hitting that, while maintaining or improving the net interest margin and continuing to bring the cost-to-income ratio down, would confirm the operating-leverage story that underpins the path to 20% returns.

If credit quality holds and the loan book keeps compounding, the re-rating from ~7x earnings toward something more appropriate for a 20%-return bank should follow, and the shares move toward — and potentially through — my base case. If the cost of risk starts climbing, or a recession arrives, the bear case becomes live quickly, and I would expect to be reducing rather than adding.

In summary, Distribution Finance Capital is a rare thing — a financial I am comfortable owning, because the business does one well-understood thing, does it well, and has a clear, credible, self-funding plan to keep doing more of it. The 2025 results were excellent, the credit quality is pristine, the growth is real, and the valuation at ~7x earnings and ~0.76x tangible book — a discount to the 75.9p of net assets behind each share — is genuinely cheap for a business targeting 20% returns. The reason I hold it modestly rather than heavily, and the reason my 80p fair value sits only modestly above tangible book rather than at the premium the return profile would justify, is the one risk that cannot be engineered away: inventory finance is cyclical, and a recession would test this book in ways it has not yet been tested. I do not see a recession imminently — which is exactly why I bought back in at 58p — but I respect that the cycle, not the execution, is what will ultimately determine whether this is a multi-year compounder or a value trap with a great-looking spreadsheet.

Disclosure: I hold a position in Distribution Finance Capital at the time of writing, bought back at around 58p. This is not investment advice — always do your own research. Read the full disclaimer at investingwithboyan.com.

If you found this useful, more analysis is available at investingwithboyan.com — or subscribe via the form in the sidebar to get new pieces straight to your inbox.