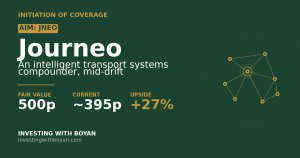

Journeo (AIM: JNEO) — Initiation of Coverage

The Quick Take

- Company: Journeo plc (AIM: JNEO) — a UK-headquartered intelligent transport systems specialist, providing the onboard sensors, passenger information displays, and software platforms that connect public transport fleets, stations and increasingly critical national infrastructure across five business lines (Fleet Systems, Passenger Systems, Infotec, Journeo A/S Denmark, and Crime & Fire Defence Systems)

- Thesis: A small-cap industrial-technology compounder that has tripled revenue over the past five years through a deliberate platform-building strategy. Five segments, each with leadership positions in their respective niches, supported by genuine UK and European public-transport spending tailwinds, and a credible medium-term ambition to nearly treble revenue again to £150m at 10%+ operating margins

- Catalyst: The recent share-price drift from 538p in September 2025 to ~395p today has reset the multiple from ~22x to ~17x trailing earnings, while the underlying business has continued to deliver record revenue, expanding gross margins, and a growing order book. The asymmetry has restored itself in our favour

- Valuation: ~395p vs my fair value of 500p (≈27% upside) — the medium-term £150m revenue ambition, if delivered, supports a materially higher fair value (~£1,000p+), but the path requires execution patience that not every shareholder has

- Key risk: AIM small-cap volatility, lumpy project revenue (the H1 2025 print showed exactly how vulnerable reported revenue is to single contract phasing — the NYC subway completion in 2024 took H1 2025 revenue down 4%), and EPS dilution from M&A-funded share placements that has been a structural drag on per-share earnings

- Position: Built progressively over the past several years; ranks as a meaningful smaller position in the portfolio

- Time horizon: 3–5 years to fully credit the £150m revenue ambition; 12–18 months for the next leg of multiple expansion if order book momentum continues

I have held Journeo for some time and the recent drift in the share price is what has prompted this proper initiation note. The shares peaked at 538p in September 2025 on the back of strong contract wins and an excellent H1 trading update; they have since drifted to around 395p — a roughly 27% drawdown over eight months. Importantly, this drift has happened without any material deterioration in the underlying business. The FY2025 results in March were record revenue, record gross profit, record gross margin and a growing order book. What has changed is the multiple, not the operational story — and that is precisely the situation where a re-initiation note earns its keep.

What Journeo actually does

In plain terms, Journeo is what happens when you put modern IoT technology onto a 1980s bus or train and a 1970s railway station, and connect the resulting signal back to a SaaS platform that someone in a control centre can actually use. The business builds, installs, services and increasingly designs the next generation of the onboard systems that make public transport function as a connected network rather than as a collection of independent vehicles.

The product set spans four broad categories. Onboard fleet systems — the cameras, telematics, passenger-counting devices, CCTV, blind-spot information, next-stop announcement displays and driver displays that go inside buses, coaches, trains, trams and specialist commercial fleets. Passenger information systems — the LED displays in bus shelters, the wayfinding totems on station concourses, the integrated information panels in airports. Rail-grade infrastructure — through Infotec, a long-established UK rail display manufacturer with roughly 80% share of UK rail network displays and a third of London Underground displays. Critical infrastructure protection — the most recent addition, through the September 2025 acquisition of Crime & Fire Defence Systems, bringing access control, intrusion detection and surveillance for high-security and critical national infrastructure.

The business sits in a quietly attractive niche. The customers are local authorities, transport operators (First Bus, Stagecoach, Arriva, Transport for London, Edinburgh Council, Cardiff Council, Danish State Railways, New York City Transit), rail operators (Network Rail, train operating companies) and a growing roster of European and North American transit authorities. The procurement cycles are long, the engineering qualification standards are high, the safety and reliability standards even higher, and once Journeo’s product is designed into a fleet or installed across a transit network, the recurring service and maintenance revenue is sticky in a way that more glamorous tech businesses can only dream about.

The market is also quietly large and structurally expanding. The UK Bus Services Act 2025 is driving a multi-year wave of investment in passenger technology. The rail sector’s transition to public ownership is driving investment into passenger experience and information systems rather than reducing it. UK and European decarbonisation targets are accelerating the replacement of older diesel fleets with newer (and more technology-rich) buses. And the broader defence and critical infrastructure budget environment is creating tailwinds for the CFDS business. Each of these is a multi-year procurement opportunity for a business of Journeo’s scale.

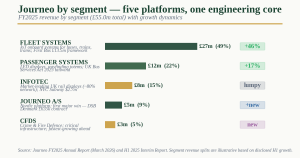

The five segments

Fleet Systems — the current growth engine and the largest segment. H1 2025 revenue grew 46% to £13.5m, driven primarily by the First Bus contract ramp and broader bus operator demand. This is the SaaS-flavoured part of the business: thousands of vehicles connected to Journeo’s platform across the UK, Ireland and Sweden, with recurring service revenue on top of the initial hardware sale. The strategic shift over recent years has been to move from purely selling hardware to selling integrated subscriptions where the hardware is part of a multi-year service contract. Margins on this segment are improving as the recurring base scales.

Passenger Systems — the street-furniture and station-display business. H1 2025 revenue grew 17% to £6.1m. This is the visible part of Journeo — the LED displays in bus shelters, the wayfinding totems, the air-quality sensors, the bus station Wi-Fi. The Cardiff Council £1.1m contract is a recent example; Edinburgh Council’s four-year extension another. UK local authority decarbonisation and bus-corridor modernisation programmes are the structural tailwind here.

Infotec — the market-leading UK rail display manufacturer, present on roughly 80% of the UK rail network and around a third of the London Underground. Recent international expansion: $2.7m New York Subway display contract, plus expanded work in Denmark. This is the highest-quality franchise in the group from a competitive-moat perspective — replicating Infotec’s 30+ years of installed base and rail-safety certifications is essentially impossible for any new entrant. H1 2025 revenue was actually down 58% (to £3.6m) due to the prior-year NYC subway contract phasing — a useful reminder of how lumpy single large contracts can make this segment look.

Journeo A/S (Denmark) — the Nordic platform acquired in September 2023. The recent Danish State Railways (DSB) contract win in March 2026 is the first major on-train system contract won by the Nordic unit since acquisition, validating the strategic case for the Nordic expansion.

Crime & Fire Defence Systems (CFDS) — the newest and least understood segment. Acquired in September 2025, CFDS extends Journeo into adjacent critical infrastructure markets — high-security access control, intrusion detection, surveillance for vital national infrastructure installations. The strategic rationale is that the engineering, integration and service-management capabilities Journeo has built for transport networks are highly transferable to other critical infrastructure verticals, and the defence/critical-infrastructure budget environment is structurally expanding. The CFDS contribution is small today but expected to be the fastest-growing segment over the next few years.

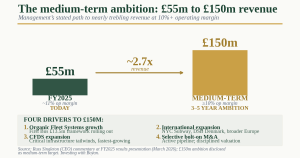

The structural opportunity: from £55m to £150m revenue

The most interesting thing the management said on the FY2025 results call was this: “we’re pretty confident that this can take us through £150m revenue with at least a 10% net operating margin.”

That single sentence is the centre of the equity story. Let me decompose what it means.

FY2025 revenue was £55.0m. The medium-term ambition is £150m — a 2.7x increase. The operating margin target is “at least 10%” — versus an FY2025 adjusted operating margin of roughly 11% on the smaller revenue base. So the company is targeting roughly trebling revenue while maintaining (or modestly improving) operating margins. The composition of that growth, as outlined by management, comes from four sources:

- Organic growth in Fleet Systems as the First Bus framework rolls out fully and additional UK operators sign up. The £10m First Bus UK framework + £3.5m London extension is the largest commercial agreement in Journeo’s history and is already partially de-risked.

- Continued international expansion through Journeo A/S and Infotec, with the recent NYC Subway and Danish State Railways wins validating the international growth thesis.

- CFDS expansion into the broader critical-infrastructure market, leveraging Journeo’s existing engineering platform.

- Selective bolt-on M&A — CFDS was the most recent example, and management has explicitly stated they are “progressing with a number of potential complementary acquisitions.”

The £150m target is, importantly, not a hockey-stick projection that requires a single transformational event. It is the cumulative effect of executing four distinct workstreams over 3–5 years, each of which is grounded in existing wins or existing strategic positioning. That makes the target meaningfully more credible than the typical “small-cap industrial promises 3x revenue” narrative deserves.

The economics, if delivered, are attractive. £150m revenue × 10% operating margin = £15m operating profit. After tax at ~22% and modest interest cost, that translates to roughly £11m of net income. On the current diluted share count of ~17.7m shares (with some further dilution likely from continued M&A activity, call it 19m shares by then), that implies adjusted EPS approaching 55–60p. At a 16–18x multiple — perfectly reasonable for a £100m+ market-cap small-cap industrial with a strong execution record — that supports a share price in the 900p–1,100p range over the 3–5 year horizon.

That is a meaningful upside from current levels. But it is also explicitly a 3–5 year story, not a 12-month catalyst. Anyone who needs the share price to deliver quarter-by-quarter will find Journeo a frustrating holding; anyone with the patience to let the platform compound will find the math attractive.

Financial shape: record revenue, expanding margins, but EPS dilution is a real issue

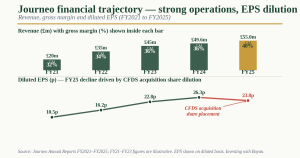

Revenue. FY2025 revenue of £55.0m grew 11% from £49.6m in FY2024. The five-year trajectory is from ~£15m in FY2020 to £55m today — close to a 4x in five years through a mix of organic execution and disciplined M&A.

Gross margin. FY2025 gross margin was 40%, with gross profit growing 23% to £21.8m on revenue growth of 11%. That margin expansion of approximately 400 basis points is the genuinely impressive operational story of the year. It reflects mix improvement (higher-margin SaaS-flavoured recurring revenue growing faster than lower-margin hardware), pricing discipline on new framework agreements, and operating leverage on a stable cost base.

Adjusted profit before tax. £5.7m, up 13% on prior year. Adjusted operating margin around 11%.

Diluted EPS. 23.83p, down from 26.29p in FY2024 — and this is the line that has caused the share-price drift. The decline is not driven by operational weakness; it is driven by share issuances funding the CFDS acquisition and earlier rounds of capital raised for growth investment. The diluted share count has expanded materially over recent years, and per-share earnings have lagged absolute earnings growth as a result.

This is the real bear point on the stock. Journeo’s M&A-driven growth model has historically been funded partially through equity placements (CFDS, MultiQ, the original Infotec acquisition all involved share issuance). Each of these has been individually accretive but cumulatively has created a structural EPS dilution headwind. The bull-case answer is that the long-term equity creation more than offsets the dilution — five-year shareholder returns of 419% suggest the math has worked historically. The bear-case answer is that any future M&A continues this pattern, and EPS growth lags revenue growth.

Balance sheet. Cash of £12.0m at year-end (down from £18.0m at H1, reflecting the CFDS acquisition). The invoice discounting facility of £2.75m is unutilised. The balance sheet is healthy and supports further bolt-on M&A without becoming financially stretched.

Cash flow. Strong operating cash conversion historically — H1 2024 cash flow was £7.59m on £25.6m revenue, a roughly 30% conversion rate. This is the cash that funds the M&A pipeline without requiring further equity raises beyond strategic acquisitions.

Valuation

At ~395p, Journeo’s market capitalisation is approximately £70m on roughly 17.7m diluted shares outstanding.

On trailing FY2025 diluted EPS of 23.83p, the trailing P/E is 16.6x. On consensus forward estimates of approximately 28–32p EPS for FY2026, the forward P/E is around 13–14x. EV/EBITDA on trailing FY2025 is approximately 9–10x, depending on EBITDA adjustments and net cash treatment. These are modest multiples for a business with this growth trajectory and franchise quality.

The recent share-price drift from 538p to 395p has compressed the multiple meaningfully. At 538p, the trailing P/E was 22.6x — a multiple that priced in flawless execution against the medium-term ambition. At 395p, the multiple is 16.6x — which prices in continued operational delivery but not the full upside scenario. That re-rating has done useful work for new money.

My fair-value framework:

- Bull case (~600–700p, 52–77% upside). FY2026 revenue grows 15–20% to £63–66m as First Bus framework fully ramps and CFDS contributes a full year. EPS recovers to 35p+ as dilution effects from FY2025 normalise. Multiple re-rates to 18–20x on improving fundamentals and continued contract momentum. Order book continues to compound. Shares retrace toward the September 2025 peak.

- Base case (~450–550p, 14–39% upside). FY2026 revenue grows ~12% to £62m. EPS recovers to ~30p. Multiple holds in the 15–17x range. Steady operational execution but no major positive surprises. Share price drifts back up to the middle of the recent trading range as the market re-acknowledges the operational quality.

- Bear case (~280–320p, 19–29% downside). AIM small-cap risk-off intensifies. Order book momentum slows. Further EPS dilution from another M&A deal that the market views as expensive. Multiple compresses to 11–13x. Share price retests the 52-week low.

Probability-weighting (35% bull / 50% base / 15% bear) gives a central fair value of approximately 500p on a 12–18 month view — roughly 27% upside from current levels. That is a respectable risk/reward profile, and importantly the bull-case scenario offers a 50%+ return while the bear-case downside is contained at around 20–25%. The asymmetry, in other words, is genuinely favourable at current levels in a way that simply was not true at 538p.

It is worth being explicit about what the 500p central fair value represents. It is a 12–18 month target that reflects multiple-recovery on continued operational execution. It is not the long-term equity value implied by the £150m revenue ambition — that, if delivered, supports a fair value closer to 1,000p+ on a 3–5 year horizon. The 500p number is the first leg; the longer-term re-rating is the second leg. New money buying at 395p is effectively underwriting the first leg with substantial optionality on the second.

Key risks

- AIM small-cap volatility. £70m market cap, single-digit-thousand daily volume, no FTSE inclusion mandate. Liquidity matters when you want to exit, and AIM-driven selling pressure can move the share price materially regardless of fundamentals.

- Lumpy project revenue. The H1 2025 print is the clearest illustration: NYC Subway phase 1 completing in 2024 took reported H1 2025 revenue down 4% despite strong organic growth in Fleet and Passenger. Single large contracts dropping in or out of a given period can make the optics look weak or strong relative to underlying trend.

- Continued EPS dilution risk. M&A funded by equity placements has been a structural drag on per-share earnings. Any future deal that requires fresh equity at depressed prices would compound this — the company’s market-cap-to-deal-size ratio matters more here than at larger businesses.

- Customer concentration. Disclosure on customer concentration is limited but the framework agreements with First Bus (UK and London) represent a meaningful portion of forward Fleet Systems revenue. Any single major customer relationship souring would have a disproportionate impact.

- Regulatory and procurement cycle risk. Local authority and transport authority budgets are politically sensitive. A change in UK government priorities, or a budget squeeze at the local level, would translate quickly into procurement delays.

- Multiple compression in a risk-off environment. Despite the recent re-rating, 16x trailing earnings is still toward the higher end of small-cap industrial valuations. In a meaningful market drawdown, the multiple could compress further.

- Integration risk on CFDS. The September 2025 acquisition is still being integrated. CFDS operates in adjacent but not identical markets to Journeo’s core, and the integration thesis has yet to be fully proven through a sustained operational period.

- Foreign currency. Increasing international exposure (Denmark, Sweden, USA) introduces FX translation noise into the GBP-reported numbers.

What I’m watching from here

Three concrete operational tests will define the next 12 months:

- H1 2026 trading update (likely July 2026) — the first reporting period that will include a full half of CFDS contribution and a full half of First Bus framework execution. The key data point is whether the order book continues to grow at the H1 2025 pace (+25% intake, +33% pipeline). If yes, the operational thesis is firmly intact and the multiple should respond.

- First Bus contract delivery milestones. The £10m + £3.5m framework agreements are the largest commercial agreements in Journeo’s history. Watch the deployment cadence in management updates — fleet rollouts at scale are operationally complex and any meaningful delays would be a yellow flag.

- Next M&A move. Management has signalled an active pipeline. The strategic question is what gets acquired and at what price. Another transformational deal at the right valuation would strengthen the platform; another large equity-funded deal at a depressed share price would compound the dilution headwind that has already driven the recent share-price weakness.

If those three boxes tick — H1 momentum, First Bus delivering, disciplined M&A — the share price should approach the upper end of my base case by end of 2026, with the bull-case scenario opening up on FY2026 results in March 2027. If order book momentum stalls or another large dilutive deal lands, the share price could revisit the bear case before fundamentals reassert.

In summary, Journeo is a high-quality small-cap industrial-technology business with a credible medium-term growth ambition, an expanding portfolio of structural tailwinds, and a recent share-price drift that has materially improved the entry-level risk/reward profile. The 27% drift from 538p to 395p has happened largely without operational justification — the underlying business has continued to deliver record revenue, expanding gross margins and a growing order book. The medium-term £150m revenue ambition is genuinely credible and, if delivered, implies a share price several multiples of current levels over a 3–5 year horizon. The near-term 12–18 month target of ~500p is supported by simple multiple-recovery on continued operational execution. For me, this fits a smaller portfolio slot with meaningful optionality, and at current levels the case for adding to existing positions on weakness is more compelling than it has been at any point in the past 12 months.

Disclosure: I hold a position in Journeo at the time of writing. This is not investment advice — always do your own research. Read the full disclaimer at investingwithboyan.com.

If you found this useful, more analysis is available at investingwithboyan.com — or subscribe via the form in the sidebar to get new pieces straight to your inbox.